Stablecoins are the backbone of DeFi, functioning as units of account, mediums of exchange, and crucially as collateral for lending protocols. However, stablecoins differ significantly in their price stability, redemption mechanisms, and risk profiles, especially with the emergence of new models. Accurate and robust pricing of stablecoins is essential for lending protocols to prevent bad debt, ensure fair liquidations, and maintain user trust.

Date

Topic

DeFi

This article presents a comprehensive framework for pricing stablecoins in DeFi lending markets, addressing the unique challenges and risks posed by various stablecoin types and the rapidly evolving landscape of decentralized finance

1. Stablecoin Taxonomy & Tokenomics

1.1 Key Stablecoin Types

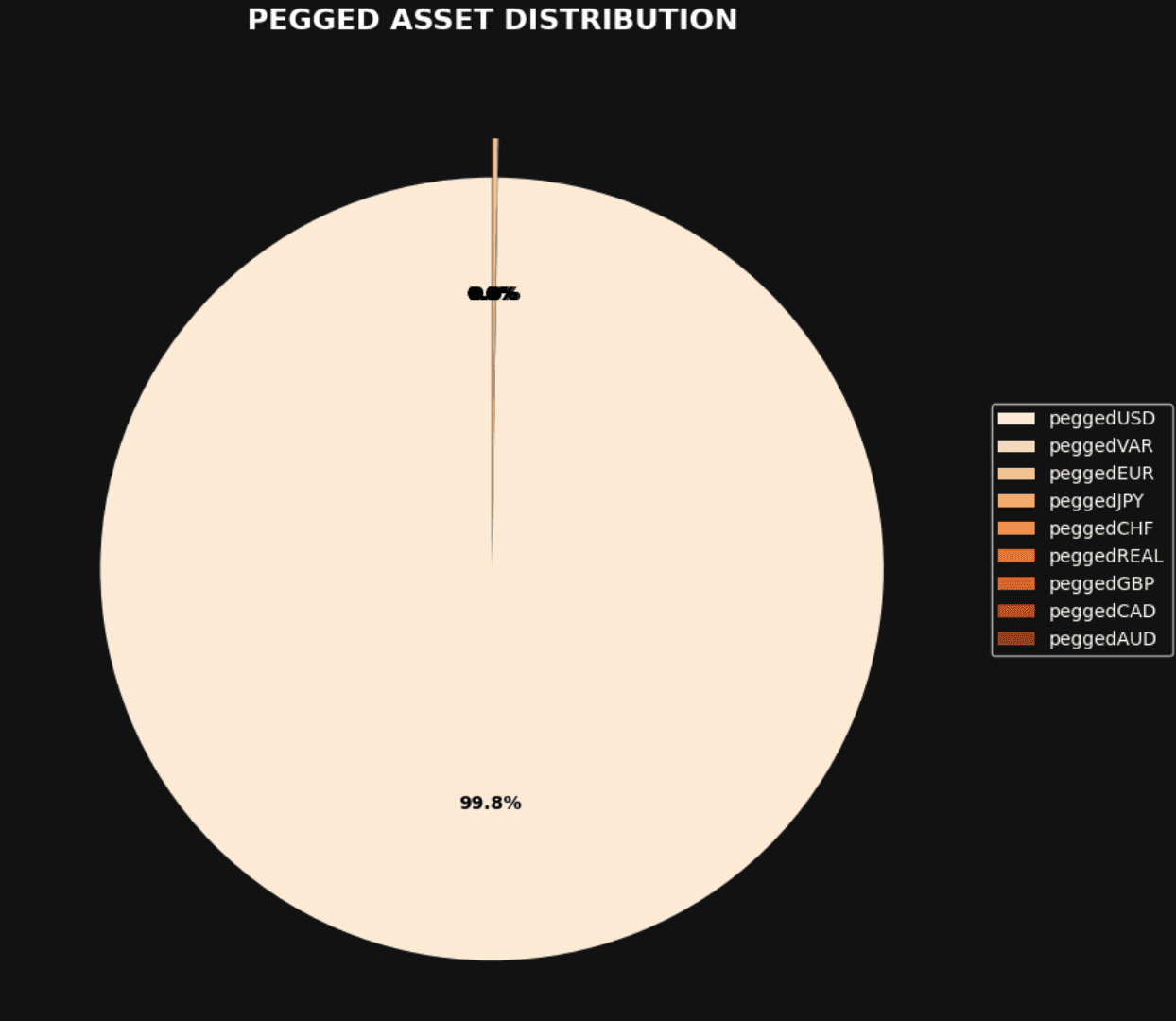

99.8% of stablecoins are USD-denominated. Source: DefiLlama |

Fiat-backed (Off-chain reserves):

Examples: USDC, USDT, USD0

Backed 1:1 by USD or equivalents held off-chain. Redemption is via centralized issuers.Crypto-collateralized (On-chain reserves):

Examples: BOLD, DOLA, LUSD, DAI, USDN (SMARDEX)

Overcollateralized with on-chain assets like ETH or LSTs. Reserves are transparent due to being on-chain. Pegs are maintained via direct redemptions and/or arbitrage, but they are capital-inefficient and sensitive to market volatility.

(Note: Descriptions here focus solely on core mechanics like collateral type and peg maintenance; they do not address factors such as overall resilience, permissionlessness, marketing positioning, or similar attributes.)Algorithmic / Hybrid:

Examples: UST, FRAX, GHO (Aave)

Use partial collateral, algorithmic mint/burn mechanisms, or protocol-set interest rates. Aim for capital efficiency but carry higher risk. UST collapsed due to reflexivity; FRAX and GHO use more nuanced hybrid models with variable collateralization or DAO-controlled monetary policies.Actively Managed:

Examples: USDe (Ethena), USR (Resolv)

Stables that involve off-chain components that require ongoing human oversight and intervention to manage hedging, custody, and risks. Sometimes backed by delta-neutral strategies (e.g., long crypto + short perps), not static reserves, often involving centralized exchanges and custodians. More capital-efficient but introduce strategy complexity and counterparty risks.Yield-Bearing Stablecoins:

Examples: wUSDN, sDAI, autoUSD, sGHO, sUSDe, sBOLD, etc.

Accrue yield or rewards to holders via different mechanisms, which make them differ greatly in terms of risk profiles and desirability as collateral for lending markets. Yield sources include staking, funding fees, lending protocols, or T-bills. Higher integration friction and smart contract risk, but improved capital efficiency when used as collateral.

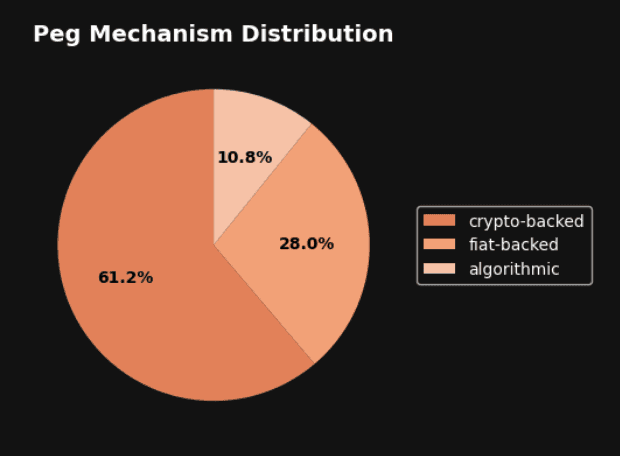

Peg-mechanism distribution, count of project numbers. Source: DefiLlama |

1.2 Redemption & Liquidity Mechanisms

Redemption and liquidity mechanisms are fundamental components to assess by any curator or lending protocol, directly impacting its stability, user trust, and overall resilience. Robust liquidity ensures that users can redeem or exit their positions efficiently, which is essential for maintaining the protocol’s solvency and preventing the buildup of bad debt.

Direct Redemption:

Can the token be redeemed 1:1 for its underlying (fiat, crypto, etc.)? Is redemption permissionless or restricted, for example by KYC? How fast can it occur? How does the protocol behave in edge cases (secondary market depeg/overpeg, mint caps lifted / added etc.) ?Secondary Market Liquidity:

Is there deep liquidity on centralized exchanges (CEXs) and decentralized exchanges (DEXs)? What are the typical spreads and slippage?Emergency Mechanisms:

Are there circuit-breakers, kill switches, or emergency redemption processes?

Without effective redemption options and deep secondary market liquidity, lending platforms risk facing liquidity crises, loss of peg for stablecoins, and ultimately, erosion of user confidence. Therefore, understanding and designing strong redemption and liquidity frameworks is crucial for the long-term health and reliability of lending protocols.

1.3 New Challenges

1.3.1 Cross-Chain & Layer-2 Liquidity

Interoperability Risks: Pricing must account for stablecoins bridged or issued across different blockchains (Ethereum, Solana, Layer-2). Liquidity fragmentation and cross-chain oracle reliability are key challenges.

Centralization Risks (Stage 0 and below): Some chains have Stage 0 status (as defined by platforms like L2Beat), meaning their sequencers are still fully centralized and controlled by a single entity. This centralization gives operators the technical ability to freeze assets or filter transactions at the sequencer level, as seen during incidents like the Linea rollup hack, where the sequencer was paused to block certain addresses and halt the network. Such risks—unique to early-stage or less-decentralized rollups—can disrupt liquidity and undermine trust in cross-chain stablecoin operations.

It’s also worth noting that there are even “stages below 0” (even though L2Beat officially stops at 0), and a few notable exceptions remain.

Layer-2 Specifics: Stablecoins on Layer-2 may require specific pricing models, taking into account the different levels of liquidity and the need to oftentimes bridge to exercise a redemption.

1.3.2 Real-World Asset (RWA) Collateralization

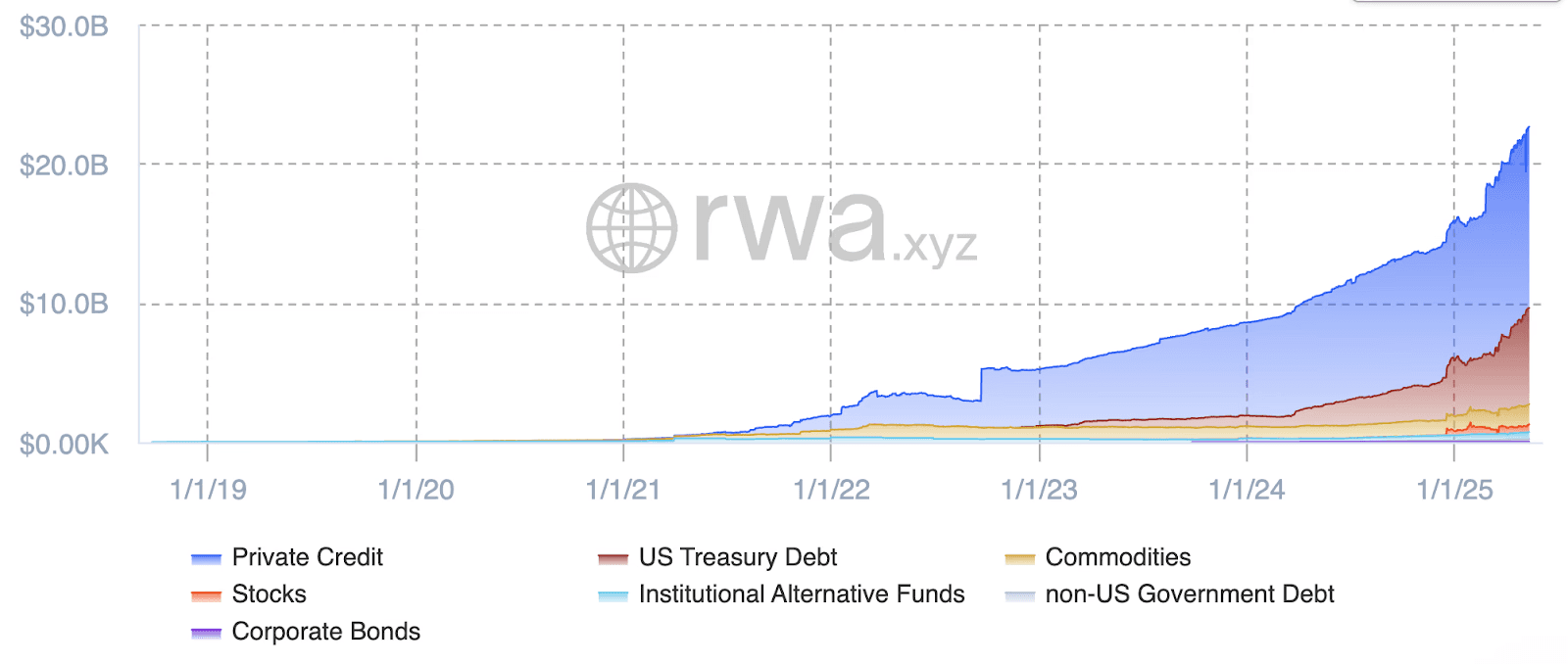

Since 2021, the total capitalization of tokenized real-world assets (RWAs) on public blockchains has surged to over $22 billion, with growth accelerating sharply in 2024 and 2025. Private credit now represents the largest share, followed by US Treasury debt and smaller allocations to stocks, commodities, and other categories. This rapid expansion highlights both the increasing demand for on-chain exposure to traditional assets and the diversification of collateral types available for stablecoins and DeFi protocols.

Total historical RWA capitalization in USD $ by underlying asset category. Source: rwa.xyz |

Valuation Complexity: For stablecoins backed by real assets (real estate, tokenized T-bills), it is crucial to assess the liquidity and real value of the collateral, as well as liquidation times.

Legal & Default Risks: Legal compliance is fundamental. If not respected, a protocol could technically be shut down or put under administration, which could cause user-panic. Additionally, delays in liquidating RWAs can lead to depreciation or losses for hybrid protocols.

It is considered a poor design choice to back an illiquid and hard-to-sell asset with something highly liquid and easy to sell-for example, consider the massive crash of USDR (1) (2). When users rushed to redeem USDR, they quickly drained the protocol’s liquid DAI reserves, leaving only illiquid real estate and native tokens as collateral. Because these assets couldn’t be sold or liquidated fast enough to meet redemptions, USDR rapidly lost its peg, plummeting to $0.50 within hours. This episode highlights the fundamental risk: if a stablecoin’s liabilities (what users can redeem on demand) are highly liquid, but its assets are not, any surge in redemptions can trigger a catastrophic loss of confidence and value.

Bonus Section: The “Yield Wars” Among Stablecoins

The landscape of decentralized finance (DeFi) has witnessed a significant evolution in recent years, with mid-late 2023 marking a period of intensified competition among yield-bearing stablecoins. In a bid to attract and retain capital, protocols are increasingly engaging in a "yield war," where they vie for liquidity by offering ever-higher Annual Percentage Yields (APYs) and pioneering innovative and sometimes risky yield-generation strategies.

This aggressive competition has led to a notable inflation of APYs across the sector. Lured by the promise of high returns, users are flocking to these protocols, inadvertently fueling a cycle of escalating risk-taking. As protocols compete for a finite pool of liquidity, the pressure to offer the most attractive yields can lead to the adoption of more aggressive and potentially unsustainable strategies.

The growing divergence between the high, yet often volatile, yields in DeFi and the more conservative returns in traditional finance has created a fertile ground for arbitrage. While these opportunities can be lucrative, they also introduce new vectors of vulnerability to the protocols. The constant search for higher yields can expose protocols to unforeseen risks, especially when market conditions shift.

For lending protocols, navigating this high-stakes environment requires a proactive and disciplined approach to risk management.

2. Risks and Mechanisms of Yield Generation

Yield-bearing stablecoins are a rapidly growing segment within decentralized finance, offering users the promise of both price stability and passive income. However, the mechanisms by which these stablecoins generate yield are diverse and complex, each introducing unique risk factors that must be carefully understood and managed, especially when these assets are used as collateral in lending protocols. This section explores the principal yield generation mechanisms, the associated risk landscape, and the critical structural features that influence both performance and safety.

Key characteristics to consider when evaluating yield-bearing stablecoins include: the source and distribution mechanism of yield, peg maintenance mechanism, type of backing, custody arrangements, regulatory status, liquidity profile and redemption cadence, governance model, risk concentration, and infrastructure (blockchain) availability. These elements collectively determine a stablecoin’s resilience and suitability as collateral.

2.1 Mechanisms of Yield Generation

2.1.1 Real-World Asset (RWA) Exposure

Stablecoins backed by real-world assets allocate their reserves to tokenized versions of traditional financial instruments, such as government bonds or money market funds. This approach seeks to harness the stability and predictability of off-chain yield sources.

How it works:

Protocols purchase or hold tokenized RWAs (e.g., treasury bills, bonds).

Off-chain interest payments are collected and distributed to stablecoin holders via on-chain mechanisms.

Key considerations:

Yield profile: Generally stable and tracks traditional finance rates.

Risks:

Dependence on centralized custodians and other trusted parties for asset management and redemption. Trust in the reports and good faith of the team.

Regulatory clarity is essential; legal uncertainty can block access to underlying assets.

Redemption and liquidity risks if assets become illiquid or inaccessible, for example in case of a bank run.

2.1.2 Crypto Derivatives and Hedging Strategies

Some stablecoins generate yield through sophisticated trading strategies in crypto derivatives markets, aiming to profit from market inefficiencies while minimizing directional exposure.

How it works:

Protocols engage in delta-neutral strategies (e.g., funding rate arbitrage in perpetual futures).

Returns are algorithmically stabilized and distributed to holders.

Key considerations:

Yield profile: Can be attractive but highly dependent on market conditions; yields may be negative in downturns.

Risks:

Market Risk: The delta-neutral hedge is relative to the derivative's quote currency (e.g.,

USDT). The strategy remains exposed to significant, unhedged losses if this quote asset were to de-peg (or go over-peg).Counterparty Risk: The strategy requires posting collateral on external venues, creating exposure to the insolvency of centralized exchanges or smart contract failures on decentralized platforms.

Execution Risk: Success is critically dependent on robust and effective rebalancing systems. It also entails reliance on the managing team's competence and the security of the asset custodian.

2.1.3 DeFi-Native Yield Strategies

A new generation of stablecoins see admins or protocol managers deploy their reserves directly into DeFi protocols, such as lending platforms or liquidity pools, to earn yield from borrower demand and trading activity.

How it works:

Collateral is supplied to DeFi protocols (e.g., Aave, Compound, Uniswap).

Yield arises from interest payments or trading fees, distributed to holders.

Key considerations:

Yield profile: Variable with demand, utilization, and trading activity.

Risks:

Sensitive to DeFi market cycles and competition; yields can compress rapidly. Adequate insurance mechanisms need to be in place in case of DeFi hacks or exploits.

Liquidity Sensitivity: The strategy's stability depends on the liquidity of all assets in the stack. A rush to redeem from a top-layer protocol can abruptly drain liquidity from a base protocol, creating systemic stress.

The design principle of such solutions is heavily based on high performance. This relentless pursuit of higher yields incentivizes a pattern of aggressive composability: a new protocol will absorb a high-yielding asset from a predecessor, layer on its own mechanisms to further amplify returns, and issue a new, re-tokenized asset to its users. While seemingly innovative, this creates a vicious cycle of compounded risk.

Each new protocol layer introduces additional vectors for smart contract vulnerabilities, counterparty failures, and liquidity mismatches, making the overall risk profile cumulative and increasingly opaque. This trend fosters a high degree of interconnected fragility within the DeFi ecosystem. Consequently, a single point of failure—whether a smart contract exploit, a de-peg event, or a liquidity crisis in a base protocol—can trigger a domino effect, leading to a cascade of redemptions and insolvencies throughout the entire dependent stack.

2.2 Principal Risks and Mitigation of Yield Generation

While yield-bearing stablecoins offer attractive opportunities for both users and lending protocols, the pursuit of yield introduces significant risks. These risks can directly impact stablecoin stability and, by extension, the solvency of protocols that accept them as collateral. Understanding and mitigating these risks is crucial for sustainable adoption.

Risks & Description

Risk | Description |

|---|---|

Strategy Decay and Yield Volatility | Fluctuating market conditions can cause rapid declines in yields, inverting borrowing costs and leading to liquidations or depegs. Overexposure during yield overestimation increases systemic fragility. |

Smart Contract and Protocol Risk | Exposure to code vulnerabilities, governance failures, or exploits in decentralized infrastructure. Complex strategies amplify risks, where minor bugs can cause cascading collateral losses. |

Counterparty and Custodial Risk | Dependence on third-party solvency for RWA backing or derivatives. Failures like fraud, regulatory seizures, or exchange insolvencies can destabilize reserves, especially without transparent auditing. |

Liquidity and Redemption Risk | Illiquid assets or congested mechanisms during stress can trigger depegs. Delayed exits lead to haircuts, eroding trust and creating sell pressure. |

Regulatory and Compliance Risk | Evolving regulations may freeze redemptions or restrict operations, with jurisdictional fragmentation complicating compliance and undermining adoption. |

Compounding and Misreporting Risk | Overstated yields or governance manipulation can hide losses, while aggressive compounding amplifies drawdowns during decay. |

Mitigation Strategies

For yield-bearing assets to be accepted as collateral across DeFi lending markets, protocols must proactively design with resilience, transparency, and composability in mind.

Here are key design practices to increase trust and usability:

Strategy | Description |

|---|---|

Conservative Yield Modeling, Insurance Fund | Use stress-tested, trailing averages for APYs to avoid inflated expectations and cushion against volatility or funding rate inversion. |

Modular Circuit Breakers & Safeguards | Embed real-time monitors and on-chain circuit breakers to mitigate surges in mint demand or redemptions, reducing systemic contagion in high-stress environments. |

Transparency & Real-Time Attestations | Integrate verifiable proofs of reserve and hedging exposure via on-chain or zk attestations. |

Smart Contract & Strategy Auditing | Conduct thorough audits to address vulnerabilities in contracts and strategies. |

Jurisdictional & Regulatory Risk Controls | Diversify RWA exposure across geographies and custodians, or avoid RWAs for DeFi-native products. |

Secondary Market Liquidity Planning | Ensure deep liquidity on AMMs and aggregators, incentivize LPs sustainably, and design redemption UX for orderly exits. |

3. Pricing Mechanisms & Resilience of Collateral

Framing the Pricing Challenge

The method by which stablecoins are priced within DeFi lending protocols is far from a trivial technical detail—it fundamentally shapes how risk is managed, how collateral is valued, and how resilient a protocol can be in the face of market stress or depegging events. Unlike traditional finance, where asset pricing often relies on regulated benchmarks or centralized market makers, DeFi protocols must operate in a decentralized, frequently volatile environment. The choice of pricing mechanism—whether based on redemption value, market price, or a hybrid approach—directly influences user trust, protocol solvency, and the ability to respond effectively to sudden market dislocations. In this section, we examine the principal pricing mechanisms used in DeFi, exploring their definitions, practical applicability, and the nuanced trade-offs each entails.

3.1 Pricing Models Used in Lending Protocols

Pricing Model | Advantages | Risks/Limitations | Recommended Use |

|---|---|---|---|

Internal Redemption Rate | Anchors to fundamental collateral value | May lag if redemptions paused or gated | Strong fiat / on-chain collaterals |

Market Price (Oracle Feeds) | Real-time updates, responsive to market events | Vulnerable to manipulation in low-liquidity markets | Highly liquid stablecoins |

Hybrid Pricing (Min/Combined) | Balances stability and market signals | More complex to implement | Riskier or yield-bearing tokens |

Hardcoded Pricing | Simple, avoids liquidations during crises | May dangerously overstate collateral value | Reserved for exceptional cases |

3.2 Extreme Scenarios & How to Respond

This subsection details specific pricing approaches under stress, including their definitions, strengths, limitations, and examples. I've structured each as a dedicated table for clarity.

3.2.1 Redemption Failure (Focus: Internal Redemption Rate)

Definition and Applicability

The internal or redemption rate refers to the value at which a stablecoin can be exchanged for its underlying collateral, as stipulated by the issuing protocol. This mechanism is most relevant for fiat-backed and crypto-collateralized stablecoins with transparent, reliable redemption frameworks, as well as yield-bearing stablecoins where internal accounting tracks accrued value like in the case of a ERC-4626 vault.

Aspect | Details |

|---|---|

Strengths |

|

Limitations |

|

Use Case Example | Protocols that are collateralized by ETH LSTs-based delta-neutral positions, USDC or USDT may reference the redemption rate to minimize risk from short-term market volatility. However, if redemptions are suspended (as seen in some historical incidents), the protocol may overstate the collateral's true market value. |

3.2.2 Liquidity Crisis (Focus: Hardcoded Pricing)

Definition and Applicability

Hardcoded pricing is extremely popular amongst emergin stablecoin protocols. It assigns a fixed value to a stablecoin (typically $1) or ERC-4626 vault token, regardless of market or redemption conditions. This is sometimes used to simplify collateral valuation, avoid oracle dependencies, or prevent cascading liquidations during market stress.

Aspects | Details |

|---|---|

Strengths |

|

Limitations |

|

Risk Notes

Hardcoded pricing is often a temporary solution or used in low-liquidity environments, but it is unsustainable for robust risk management. Protocols should communicate risks transparently and consider fallback mechanisms, such as circuit breakers or governance interventions, when market conditions diverge from the hardcoded value.

3.2.3 Market Price (Oracle Feeds)

Definition and Applicability

Market price mechanisms aggregate real-time prices from exchanges (CEX/DEX) via decentralized oracles (e.g., Chainlink, Redstone). This approach is broadly applicable to all stablecoins, especially those with significant on-chain and off-chain liquidity.

Aspect | Details |

|---|---|

Strengths |

|

Limitations |

|

Use Case Example | Protocols like Aave and Compound rely on oracle feeds to value stablecoins and trigger liquidations. This ensures rapid response to depegs but exposes the protocol to oracle manipulation or flash loan attacks in low-liquidity environments. |

Previous Event

This was evident during the USDC depeg in March 2023, when USDC briefly fell below $0.90 due to concerns over reserve exposure to Silicon Valley Bank. Protocols relying solely on market price oracles, such as Aave and Compound, faced pressure as collateral valuations deviated sharply from redemption values, risking unnecessary liquidations.

Similar issues have occurred in smaller stablecoins like MIM or FEI, where thin liquidity made oracle-driven pricing highly volatile during periods of stress or manipulation.

3.2.4 Hybrid/Combined Pricing (Novel Approach)

Definition and Applicability

Hybrid pricing is not yet standard in stablecoin protocols, and its usage remains rare—but when implemented, it offers substantial flexibility and resilience. Under this approach, the protocol typically uses the market price derived from oracle feeds, but in times of extreme liquidity disruption or peg dislocation, it defers to an internal redemption value conditionally to the availability of reserves, or similar. Decisions are based on predefined conditions—such as liquidity depth, redemption availability, or reserve capacity—making hybrid pricing particularly relevant in current markets.

Aspect | Details |

|---|---|

Strengths |

|

Limitations |

|

Use Case Example | Hybrid pricing—selectively combining oracle-based market prices with issuer redemption value—offers a path toward more resilient stablecoin valuation frameworks. It provides real-time sensitivity while guarding against extreme dislocations. But it demands thoughtful design around fallback logic, transparent thresholds, and trust in both oracle and redemption integrity. |

Choosing the Right Mechanism

No single pricing mechanism is universally optimal. Each approach offers distinct advantages and exposes protocols to specific risks, particularly under stress scenarios or during market dislocations.

For curators, the key is to align the pricing mechanism that reflects both the stablecoin’s inherent risks and real-world liquidity constraints. This demands an intimate understanding of the token’s behavior under extreme edge cases, such as cascading liquidations, redemption halts, or collateral depegs, to align pricing with the protocol’s risk thresholds and real-time liquidity dynamics. Only through rigorous stress-testing and scenario analysis can curators ensure mechanisms remain robust amid volatility.

4. Extreme Scenarios & Edge Cases

Stablecoins serve as critical infrastructure within DeFi. This section examines exceptional scenarios that can disrupt stablecoin stability, analyzes their impact on DeFi lending protocols, and proposes mitigation strategies based on empirical evidence and computational modeling. Understanding these edge cases is essential for designing robust pricing oracles that maintain protocol solvency while preserving liquidity during market stress.

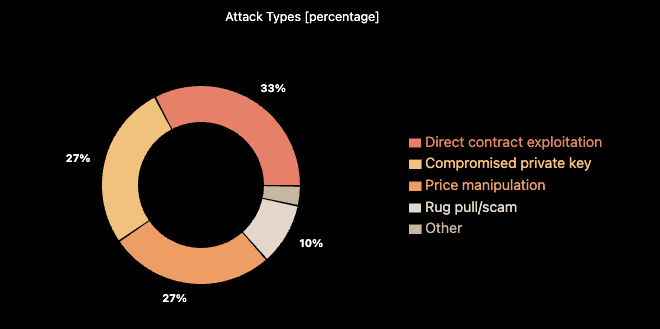

From 2016 to 2023, between the top 100 DeFi Hack, 27% of exploits were Price Manipulation attacks for a total of $846,623,000 USD. Source: HALBORN Report |

4.1 Redemption Failure

Redemption mechanisms represent the fundamental value proposition of most stablecoins, particularly those backed by fiat currency reserves. When this core function becomes compromised, the consequences can rapidly cascade throughout DeFi ecosystems.

Definition and Mechanism:

Redemption failures occur when stablecoin issuers suspend or restrict users' ability to exchange their tokens for underlying collateral assets. Such failures may result from regulatory intervention, operational disruptions, or questions about reserve adequacy. While the "official" redemption rate typically remains pegged at $1, secondary market prices often rapidly diverge as market confidence erodes.

Historical Evidence:

Event | Details |

|---|---|

Tether (USDT) Depegging (2018) | Amid concerns about USD reserve transparency, USDT briefly traded at $0.85 on secondary markets despite a theoretical $1 redemption value. |

TerraUSD (UST) Collapse (2022) | Maintained algorithmic mint/burn mechanics as market prices entered a death spiral, eventually rendering the token valueless. |

Impact on Lending Protocols:

When redemption failures occur, lending protocols face asymmetric risks:

Protocols using redemption rates may accept the stablecoin at par value after markets discount it, creating solvency risks.

Protocols relying on market prices may trigger unnecessary liquidations during temporary disruptions.

4.1.2 Mitigation Strategies

To address redemption failure risks while maintaining operational flexibility, protocols should implement safeguards tied to quantifiable impairment thresholds rather than subjective assessments:

Hybrid Pricing With Clear Impairment Triggers

Transition from redemption-rate to market-derived pricing only when predefined impairment criteria are met:

Trigger Criterion | Description/Details |

|---|---|

Redemption Delays | >6 hours (matching Tether’s historical processing times during stress) |

Redemption Fees | Exceeding 0.1% (benchmarked against industry standards) |

Daily Redemption Volume | Surpassing 150% of 30-day averages (detecting bank-run patterns) |

Transparent Circuit Breakers

Adopt ERC-7265-compliant mechanisms to:

Mechanism/Action | Description/Details |

|---|---|

Pause New Borrowings | If redemption delays persist >12 hours |

Temporarily Custody Outflows | During cooldown periods |

Public Real-Time Status Updates | Via on-chain events |

Dynamic Risk Parameter Adjustments

Automatically modify collateral requirements based on:

Adjustment Basis | Description/Details |

|---|---|

Redemption Health | Reduce LTV by 15% if redemption fees exceed 0.05% |

Market Volatility | Implement volatility-adjusted LTV caps (e.g., 50% max during >30% ETH price swings) |

Collateral Composition | Apply haircuts to assets with >24h liquidation timeframes |

Redemption Metrics as Leading Indicators

Integrate redemption analytics into risk models:

Metric | Description/Details |

|---|---|

On-Chain Redemption Queues | Monitor pending transactions exceeding protocol reserves |

CEX/DEX Spreads | Trigger alerts when secondary markets discount stablecoins by >2% |

Reserve Attestation Lags | Deprecate pricing if audits are >72h overdue |

This Strategy balances responsiveness with anti-fragility, using verifiable on-chain/data-driven triggers rather than discretionary judgments. By anchoring adjustments to observable market realities (e.g., Tether’s $0.85 depeg, USDC’s March 2023 liquidity crisis), protocols can mitigate reflexive panic while maintaining solvency.

4.2 Liquidity Crisis/Crunch

Liquidity represents the lifeblood of stablecoin ecosystems, enabling price efficiency and market functionality. When liquidity suddenly evaporates, even fundamentally sound stablecoins can experience severe price dislocations.

Definition and Mechanism:

A stablecoin liquidity crisis occurs when market depth diminishes below critical thresholds, typically during periods of market stress or panic. This phenomenon can manifest on both centralized exchanges (CEXs) and decentralized exchanges (DEXs), with particularly severe impacts on automated market maker (AMM) pools where imbalanced reserves can create pricing anomalies.

Historical Evidence:

Event | Details |

|---|---|

Black Thursday Crash (March 2020) | Ethereum prices plummeted, leading to mass liquidations in MakerDAO vaults and unprecedented DAI demand, spiking its price to $1.12. Exacerbated by network congestion preventing arbitrage. |

LUSD Overpegs | Traded at ~$1.10 during extreme demand, risking cascading liquidations in protocols accepting overpegged stablecoins if peg corrects abruptly. |

Current Vulnerabilities:

Liquidity fragmentation across DeFi represents a growing systemic issue. According to recent data, the demand for liquidity now vastly outstrips available capital across the ecosystem. Some stablecoin protocols have excessively concentrated incentives and as a consequence user activity in lending platforms rather than liquidity pools. For instance, a stablecoin protocol in May 2025 had approximately >90% of its token supply locked in lending protocols, with just two vaults on the same lending platform controlling 47% and 44.5% of the total supply respectively. This concentration creates extreme vulnerability to liquidity shocks, as redemption demands could quickly outstrip available market depth.

A screenshot of the token holders (see below, addresses blurred for neutrality) clearly illustrates this extreme concentration on just two addresses. Furthermore, this project had a design which limited redemptions to $100,000 per week per address, which makes the scenario even more dangerous given that the total value locked (TVL) was around $60 million as shown in the screenshot. This combination of concentration and restricted redemption capacity significantly increases the risk of severe depegs and forced liquidations during periods of market stress.

4.2.1 Mitigation Strategies

Solutions like Euler Swap can mitigate such scenarios, beacuse idle liquidity in lending markets can be made swappable. Otherwise, liquidity crunches demand protocols to balance market realism with anti-fragility. Drawing lessons from historical overpegs (e.g., DAI at $1.10 in 2020, LUSD at $1.08 in 2021) and systemic concentration risks, the following safeguards are critical:

Strategy | Description/Details |

|---|---|

TWAP-Based Pricing | Smooth volatility using 6-12 hour time-weighted average prices (TWAPs) to prevent flash-crash liquidations while maintaining arbitrage incentives. |

Liquidity Threshold Triggers | Deem oracle feeds unreliable if 24-hour volume falls below $10M or market depth drops under $2M, pausing volatile asset collateralization. |

Diversified Oracle Systems | Aggregate data from ≥5 CEXs and ≥3 DEXs, excluding pools with <$5M TVL to avoid manipulation. |

Redemption Rate Fallbacks | Automatically revert to protocol-level redemption prices during sustained dislocations (>2% deviation for 6+ hours). |

Liquidity resilience hinges on protocols preemptively addressing concentration risks, such as the >90% supply locked in two lending vaults case mentioned before, while dynamically adapting to market stress. By anchoring pricing to verifiable liquidity metrics rather than ephemeral market signals, protocols can mitigate reflexive panic and maintain stability. Hybrid mechanisms that blend TWAP smoothing, redemption fallbacks, and liquidity-tiered collateral requirements offer a robust defense against both overpeg spirals and underpeg bank runs.

Appendix: Oracle Design Trade-offs: Balancing Security and Market Responsiveness

In DeFi systems, oracles serve as critical infrastructure that bridges off-chain pricing data with on-chain protocols, fundamentally impacting system security. A key challenge in oracle architecture: balancing resistance to price manipulation against timely detection of legitimate market shifts.

Exponential Moving Averages as Defense Mechanisms:

Many DeFi protocols employ exponential moving averages (EMAs) to smooth price data and mitigate short-term manipulation attempts. Our computational simulations, modeled on Uniswap v2-style AMMs, quantify three critical relationships:

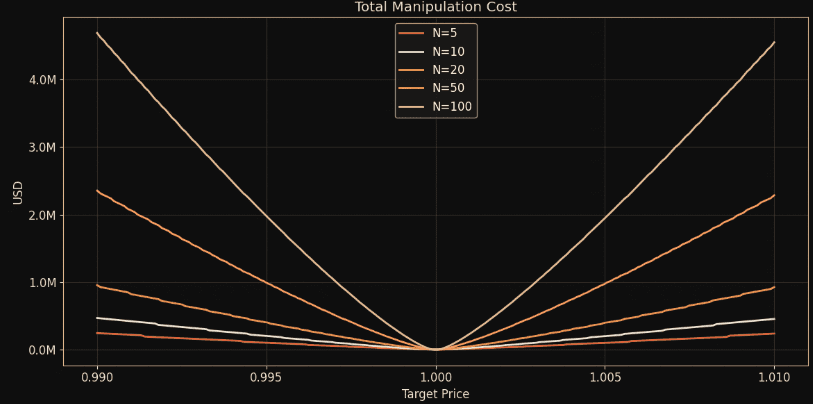

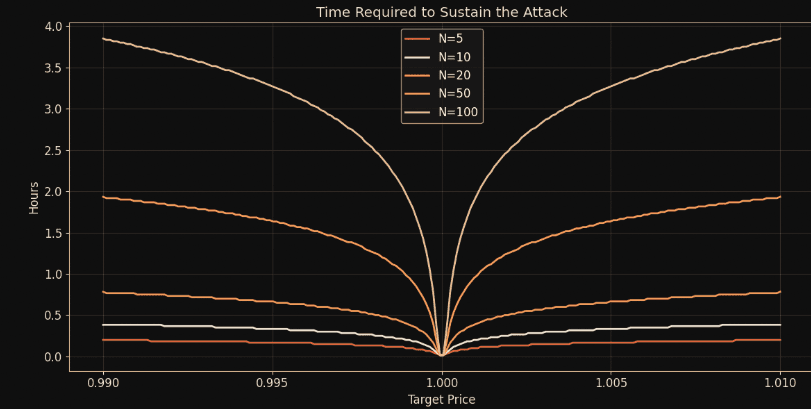

EMA Window Size vs. Attack Cost:

Larger time windows exponentially increase the capital required to successfully manipulate prices, as shown in Figure 1a & 1b. The simulation reveals that manipulation costs scale with both the width of the EMA window and the depth of market liquidity.

Figure 1a: Total capital required (USD) to manipulate the oracle price as a function of the target price deviation, for different EMA window sizes (N)

Figure 1b: Corresponding time (in hours) an attacker must sustain the manipulation to maintain the targeted price deviation.

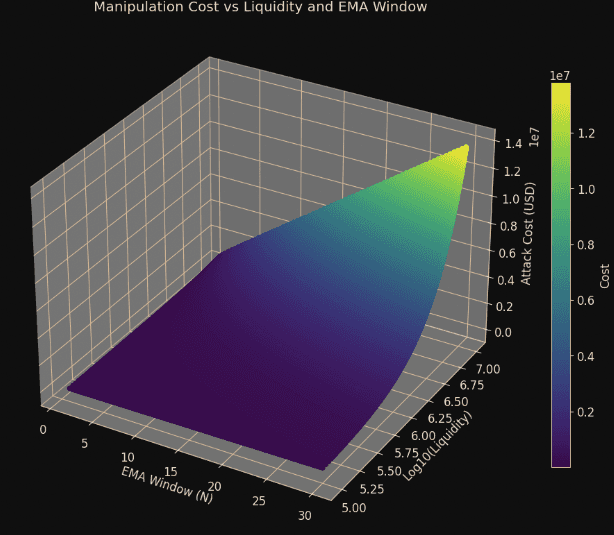

Market Depth as Defense:

Liquidity depth serves as a natural deterrent against price manipulation, with deeper pools requiring substantially more capital to influence prices. As demonstrated in Figure 2, the log of liquidity exhibits an exponential relationship with attack costs.

Figure 2: Simulated manipulation cost as a function of liquidity (log scale) and EMA window size. Deeper liquidity and wider EMA windows exponentially increase the attack cost required to manipulate the oracle price.

Volatility and Manipulation Impact:

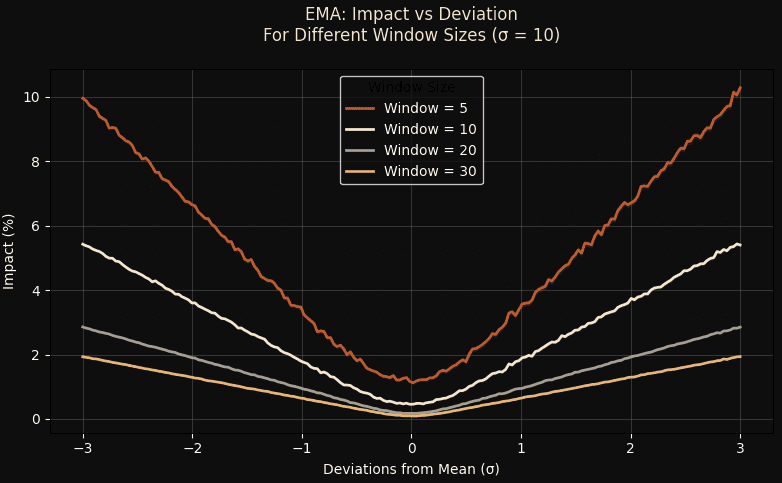

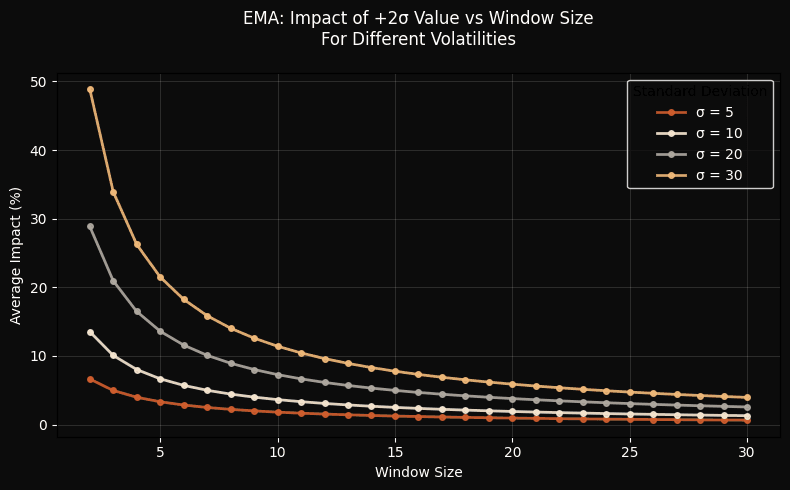

Higher market volatility creates a more permissive environment for price manipulation. Figure 3 illustrates how larger EMA windows significantly mitigate the impact of price outliers across different standard deviation ranges.

Figure 3: Simulated effect of price manipulation across σ deviations on EMA-based feeds. Wider windows significantly mitigate the impact of outliers.

Figure 3 bis: Simulated impact of a +2σ price shock manipulation on EMA oracle price feeds across different price simulated volatilities. Larger windows clearly reduce manipulation effectiveness and increase its cost to maintain it

These simulations reveal inherent tensions in oracle parameterization. Larger EMA windows enhance short-term resistance to manipulation but introduce dangerous lags in responding to genuine market shifts. Similarly, deeper liquidity pools exponentially raise attack costs, acting as a natural deterrent.

Optimizing Oracle Design:

The optimal EMA window size depends on multiple factors, including underlying asset volatility, market depth, and protocol risk tolerance. Our simulations suggest that for most stablecoins, EMA windows of 15-20 price points strike an effective balance between manipulation resistance and responsiveness to legitimate market conditions. For lending protocols specifically, slightly longer windows (20-30) may be preferable given the asymmetric risk of accepting compromised collateral.

5. Practical Pricing Guidelines

Stablecoin pricing in DeFi lending protocols is a dynamic, high-stakes process that cannot be reduced to a simple “set and forget” approach. Market conditions, protocol mechanics, and external risks evolve rapidly, requiring both robust technical tools and vigilant monitoring and oversight. The following guidelines synthesize best practices for collateral valuation, risk management, and protocol governance, emphasizing the need for continuous monitoring and adaptive controls. Even with advanced automation, human judgment and caution remain indispensable, as both technical and governance failures can—and do—occur.

General Principles

Principle | Description/Details |

|---|---|

Conservative Valuation | Always value stablecoin collateral at the lower of either the internal redemption rate or the prevailing market price. This approach minimizes the risk of overestimating collateral value during periods of stress or depeg events. |

Restrictive Borrowing Policies | Disallow borrowing against unstable or depegged stablecoins, or permit it only at very low loan-to-value (LTV) ratios. Apply higher interest rates to borrowing against riskier stablecoins to discourage excessive leverage and limit protocol exposure to bad debt. |

Redemption Health Monitoring | Continuously monitor the redemption process. If redemptions are paused, delayed, or otherwise impaired, immediately default to using the market price for collateral valuation. This prevents the protocol from relying on stale or theoretical values. Apply additional haircuts to stablecoins that exhibit opacity in backing assets, centralized control over reserves, or legal uncertainties around redemption rights. |

Secondary Market Liquidity Assessment | Regularly assess liquidity on both centralized and decentralized exchanges. If liquidity is thin or fragmented, apply additional haircuts to collateral value or consider freezing affected markets until conditions normalize. |

Direct Redemption Access and Oversight | Protocols should strive for direct access to redemption mechanisms, or at minimum, maintain transparent and real-time oversight of the assets backing each stablecoin. This reduces reliance on third parties and enhances risk detection. |

Yield-Bearing Stablecoins | For yield-bearing stablecoins, price collateral as the product of the underlying asset price and the protocol’s exchange rate. However, cap the recognized growth rate and monitor closely for anomalies or discrepancies in reported yields. |

Composability Risk Management

DeFi protocols are highly composable, often relying on other protocols for pricing, yield, or custody. While this enables innovation, it also introduces cascading failure risks. Limit exposure to deeply composable assets or strategies, implement circuit breakers for dependencies, and regularly audit inter-protocol interactions to reduce systemic fragility.

Protocol Implementation

Component | Description/Details |

|---|---|

Oracles | Utilize reputable oracle providers. For new or illiquid stablecoins, aggregate data from all available sources, including DEX time-weighted average prices (TWAPs), to mitigate manipulation risk and ensure robust price discovery. |

Circuit-Breakers and Killswitches | Implement automated circuit-breakers (CAPO/killswitch mechanisms) that can freeze markets, reduce LTVs, or trigger emergency procedures if the stablecoin price deviates beyond a predefined threshold (e.g., >X%) from its redemption value. This limits contagion and protects protocol solvency during extreme events. |

Governance and Risk Controls | Empower protocol governance and risk teams with the authority to rapidly adjust key parameters—such as haircuts, LTVs, and accepted price sources—in response to evolving market conditions. Rapid, transparent decision-making is critical for crisis management. |

Ongoing Vigilance and User Caution

It is essential to recognize that even the most sophisticated pricing frameworks and automated controls are not infallible. Oracles can fail or be manipulated, governance processes can be slow or corruptible, and human error remains a persistent risk. As such, both protocol operators and users must exercise ongoing vigilance. Continuous monitoring, stress testing, and a culture of prudent skepticism are necessary to maintain protocol integrity and user safety.

6. Recommendations for Lending Protocols

General Recommendations

Adopt a hybrid pricing model using both internal rates and robust market oracles.

Implement circuit-breakers and Killswitches to freeze or limit borrowing during extreme price dislocations or redemption failures.

Apply conservative LTVs and haircuts for new, illiquid, or yield-bearing stablecoins.

Continuously monitor redemption and liquidity health-automate alerts for anomalies.

Require regular audits and transparency from stablecoin issuers, especially for yield-bearing models.

Engage with risk providers for ongoing scenario analysis and parameter tuning.

General Risk Parameters Recommendations

To effectively minimize bad debt when using stablecoins as collateral, lending protocols must adopt a dynamic, tailored risk management framework. Here are the essential principles to follow:

Key Risk Management Principles

Header 1 | Header 2 |

|---|---|

Adaptive LTV Ratios (70–95%) | Calibrate loan-to-value ratios based on the specific characteristics of each stablecoin. Consider factors such as asset backing, redemption mechanisms, historical stability, and market evolution. |

Dynamic Haircuts (5–30%) | Implement variable haircuts that reflect the volatility profile and redemption risks of each collateral type. Regularly update these parameters through stress testing and scenario analysis. |

Liquidity-Based Collateral Factors (60–90%) | Adjust collateral factors in line with real market depth and trading volumes. Cap exposure to lower-liquidity stablecoins (e.g., <10% of total collateral) to avoid concentration risk. |

Robust Oracle Infrastructure | Use multiple, independently audited price oracles with fallback mechanisms for less liquid or emerging stablecoins. Ensure real-time, reliable pricing to safeguard against manipulation or data outages. |

Proactive Liquidation Triggers | Set high collateralization ratios (105–130%) and swift liquidation processes to minimize losses during depegs or market shocks. |

Diversification and Concentration Limits | Avoid overexposure to any single stablecoin or protocol. Diversify collateral pools to enhance overall system resilience. |

Continuous Monitoring and Auditing | Regularly audit smart contracts, governance frameworks, and asset backing (with a focus on redemption and hedging strategies). Monitor on-chain and off-chain metrics to detect emerging risks. |

Comprehensive Stress Testing | Simulate extreme market events (e.g., 50% crypto crash, redemption failures, market freezes) to ensure protocol solvency and robustness. |

Why Customization is Essential

Risk parameters should never be one-size-fits-all. Each stablecoin—and each protocol—requires a bespoke approach, considering its size, redemption mechanisms, historical performance, and ongoing evolution. This is a complex, ongoing task that demands specialized expertise and robust tooling. Attempting to manage these risks alone can expose protocols to significant vulnerabilities.

Given the complexity and potential risks involved, it is highly recommended to consult with experienced professionals when designing and implementing stablecoin risk management systems. Attempting to handle these challenges without expert guidance can expose protocols to significant vulnerabilities and financial losses. At Telos C, we offer specialized advisory and risk management services to help protocols navigate these complexities and build robust, secure DeFi platforms.

Conclusion

Stablecoin pricing in DeFi lending is a nuanced, high-stakes challenge. By combining internal redemption rates, robust market oracles, and dynamic risk management tools (such as circuit breakers and killswitch mechanisms), protocols can better protect themselves and their users from insolvency, manipulation, and depegging events.

This framework serves as a reference for listing protocols and governance committees, aiming to ensure informed, resilient, and transparent integration of stablecoins as collateral in DeFi.

—————————————————————————————————————————————

Need Expert Support?

At Telos Consilium, we specialize in advanced collateral risk management and parameter optimization for DeFi protocols.

Explore our services at telosc.com and book a call to discuss how we can tailor a risk framework to your needs.

Related articles

TeloSkills: A Free Web3 Due Diligence Skill for Claude

Coinshift USPC & iUSPC - Comprehensive Due Diligence

MainStreet – Comprehensive Due Diligence

Introducing the Kinky IRM: Enhancing Interest Curves

Risk Curation Methodology for DeFi Yield Optimization

Meet IRMaster, The Effortless Interest Rate Manager for Liquity v2 & Forks

Stablecoins as Collateral: Pricing Guidelines

Introducing the Kinky IRM: Enhancing Interest Curves

Meet IRMaster, The Effortless Interest Rate Manager for Liquity v2 & Forks