Risk Assessment & Due Diligence

Date

Topic

Due Diligence

WARNING - Important Update, June 2026

This report was originally prepared based on the information available to us around February / March 2026. It should now be read strictly as a historical snapshot of how MainStreet was functioning at that time, and not as a current accurate description of MainStreet, msUSD, msY, or any related market.

Since early June 2026, our research with multiple independent DeFi participants, curators and infrastructure providers has found information that materially changes our view of the project. The concerns raised are not limited to ordinary strategy or market risk. They go to the core of the project’s reserve backing, team identity, yield generation, redemption mechanics, reported TVL and market activity.

Several counterparties reported unresolved questions around who actually controls MainStreet. Individuals who had appeared to represent the project were later described as not knowing who the actual founders were, while key operational roles appear to have been handled through anonymous or semi-anonymous Telegram accounts.

The most serious concern relates to reserves. MainStreet was reportedly around $80M TVL when these issues surfaced, yet multiple parties were unable to obtain satisfactory reserve verification or venue-level reconciliation. Accountable, the reserve verification provider, stated that MainStreet had shut down access to its instance shortly after onboarding, resisted granular reserve disclosure, and later failed to prove reserves despite being given substantial latitude. Accountable has since terminated its relationship with MainStreet.

Additional concerns were raised around a stable 12% displayed APY, the absence of clear realized-yield reconciliation from venues such as Deribit and Binance, and limited evidence of a functioning redemption pipeline. On-chain reviewers also identified coordinated-looking wallet clusters across Morpho and Pendle, including exchange-funded wallets with similar single-purpose activity, apparent “TVL deal” behavior, an unverified Morpho vault, a separate 91.5% LLTV msY/USDC market, and an “alpha wallet” active across multiple MainStreet-related venues. Key questions around who controlled these wallets, who deployed the unverified markets, and where the liquidity originated remained unanswered.

Based on the information now available, we no longer believe the original report should be relied upon for any current investment, lending, curation, integration or risk decision. We cannot conclusively determine intent from the information available, but we believe the risk of fraud, reserve shortfall, non-organic TVL or rug-like behavior is now material.

We are keeping the original report online for transparency and historical context. However, this update supersedes the original analysis. Readers should treat the original DD as a record of what was known and represented to us at the time, not as a live recommendation or validation of the project as it exists today.

Executive Introduction: Product and Value Proposition

MainStreet is a platform delivering yield infrastructure designed to provide structured access to institutional strategies. The flagship product is msY (MainStreet Yield) - which aims to turn CME index box spreads into market-neutral, USD-denominated yield.

msUSD is instead a dollar-pegged token that serves as the base asset in the ecosystem. Each token is backed by USDC.

The protocol separates on-chain accounting and redemption logic from off-chain execution and clearing infrastructure, allowing users to gain exposure to regulated market yield strategies without directly interfacing with prime brokers, FCMs, or CME membership structures.

The core value proposition is threefold. First, it provides access to implied financing rates embedded in CME options markets, which are traditionally available only to institutions with prime brokerage and clearing relationships. Second, it wraps this exposure in a tokenized ERC-4626 structure, enabling composability, transparent NAV accounting and programmable redemption mechanics. Third, it introduces a Coverage Ratio and insurance framework intended to absorb mark-to-market volatility and mitigate run-risk dynamics during stress events.

Key Takeaways

Institutional yield strategy wrapped in DeFi infrastructure.

MainStreet tokenizes access to institutional derivatives financing strategies by packaging CME index options box spreads into an ERC-4626 vault (msY), allowing users to access implied financing rates traditionally restricted to institutional trading desks.Hybrid architecture combining on-chain accounting and off-chain execution.

Smart contracts manage issuance, redemption logic, and accounting, while strategy execution occurs off-chain through a derivatives stack involving FalconX (prime/execution), Marex (FCM clearing), and CME. This improves composability but introduces operational and counterparty dependencies.Yield derived from CME options box spreads.

The strategy captures implied financing rates embedded in options markets using box spreads. While theoretically deterministic at expiry, interim mark-to-market movements, margin requirements, and liquidity conditions introduce path-dependency risk.Counterparty concentration is a key structural risk.

Execution and margin operations currently rely primarily on the FalconX → Marex clearing path. While CME clearing reduces bilateral counterparty risk, operational continuity still depends heavily on the prime and FCM layers.Leverage is policy-bounded but materially affects solvency dynamics.

The strategy operates within a target leverage range of roughly 2×–4× with a hard cap around 4.25×. Stress modeling indicates that relatively small mark-to-market shocks can temporarily push the Coverage Ratio below 100%, even if positions converge to deterministic payoffs at expiry.Coverage Ratio and insurance fund act as solvency buffers.

The protocol maintains an insurance fund designed to absorb losses and restore coverage in stress scenarios. Soft and hard triggers define when de-risking actions or insurance deployment may occur.Redemption architecture prioritizes systemic stability over instant liquidity.

Redemptions follow a request-and-claim process with cooldowns and caps. The design reflects the liquidity constraints of derivatives positions and aims to reduce bank-run dynamics during drawdowns.Governance currently relies on multisig control without timelocks.

Key protocol parameters and upgrades are controlled by a Gnosis Safe multisig. While actions are auditable on-chain, the absence of timelocks increases reliance on operational discipline and governance transparency.Protocol growth has been rapid but concentrated.

TVL expanded from roughly $7–8M to over $22M within ~6 weeks, with inflows appearing episodic and driven by large allocators rather than organic retail demand.Stable yield appears to be the primary adoption driver.

Reported yields have remained in the ~9.5%–12% range, which likely explains recent capital inflows despite the structural complexity and risk profile of the strategy.

1. Organization, Legal Structure, and Accountability

1.1 Entity and Jurisdiction

The issuer entity is Main St Finance Ltd, incorporated in the British Virgin Islands. The team states that its activities fall under what they interpret as a BVI token issuer exemption, meaning that issuing tokens without custody, exchange, or transfer services does not require registration as a VASP. This interpretation has not been accompanied by a publicly released formal legal opinion letter classifying msUSD or msY as non-securities or non-derivatives. The team indicates such opinion could be obtained if required for listing or regulatory clarification.

US persons are restricted from minting and redeeming. Additional sanctioned jurisdictions are restricted in accordance with compliance policy. Dispute jurisdiction is stated as BVI.

Legal posture is clarified as follows: Main St Finance Ltd (BVI) relies on the BVI VASP ‘token issuer exemption,’ under which issuing tokens without providing custodial, exchange, or transfer services does not require VASP registration. The issuer does not custody user assets or private keys. US persons are restricted from minting and redeeming, and dispute jurisdiction is BVI. No formal opinion letter has yet been published, though the team indicates one may be obtained if required for exchange listings.

1.2 Execution, Prime, Clearing, and Custody Relationships

MainStreet’s core yield strategy is implemented through regulated derivatives infrastructure centered on CME index options markets. The architecture separates execution intermediation, prime brokerage functions, clearing, custody, and on-chain accounting into distinct operational layers. This separation improves structural transparency but creates identifiable counterparty concentration points that must be evaluated independently.

Execution is routed through FalconX, which operates as the protocol’s prime brokerage and execution intermediary. In this role, FalconX provides institutional trade routing, liquidity sourcing, margin coordination, and operational access to derivatives venues. FalconX serves as the interface between MainStreet and the clearing stack, facilitating trade negotiation, routing, collateral communication, and execution logistics. While FalconX is not the clearing counterparty, it represents a critical operational dependency because it intermediates order flow and margin interaction.

Clearing is performed by Marex, which acts as a registered Futures Commission Merchant (FCM). An FCM is a CFTC-regulated intermediary authorized to accept customer futures and options orders, hold and manage margin collateral, and clear trades through a derivatives clearinghouse such as CME. The FCM administers initial margin (IM), variation margin (VM), collateral eligibility rules, and liquidation protocols. It is also responsible for maintaining customer funds under regulatory segregation frameworks, including CFTC Rule 1.20 and related protections governing how customer assets must be separated from firm capital.

This role is structurally critical. Although positions are ultimately cleared at CME, customer collateral and legal account relationships exist at the FCM layer. In an insolvency scenario, the treatment of funds, portability of positions, excess margin recovery, and timing of distributions depend primarily on the FCM account structure and governing documentation rather than on the clearinghouse itself. Clearinghouse centralization reduces bilateral counterparty exposure but does not eliminate operational and legal dependency on the FCM.

At the venue layer, CME (Chicago Mercantile Exchange) operates as the central clearinghouse where index options positions are novated and margined. CME clearing reduces bilateral counterparty risk by standardizing margin requirements and interposing the clearinghouse between counterparties. However, the protective effect of clearing must be framed correctly: it mitigates direct counterparty default exposure, but margin discipline, liquidity responsiveness, and insolvency waterfall mechanics remain FCM-dependent.

The operational exposure chain can therefore be summarized as:

MainStreet → FalconX (prime / execution layer) → Marex (FCM clearing member) → CME clearinghouse.

While CME clearing provides systemic safeguards and standardized margin frameworks, the immediate operational and counterparty concentration resides at the FalconX and Marex levels. Execution continuity, collateral mobilization, hedge adjustments, and stress-time responsiveness depend on these relationships. At present, clearing exposure appears concentrated through this single FCM path, with diversification described as a forward-looking objective rather than a currently implemented safeguard.

In addition to CME-cleared execution, the team discloses that certain box spreads may be executed OTC through FalconX. In this context, OTC execution refers to negotiated bilateral pricing facilitated by the prime intermediary rather than direct placement on CME’s central limit order book. OTC facilitation may allow improved liquidity access or pricing efficiency for large notional execution, but it introduces additional reliance on prime-level controls, execution transparency, and post-trade reconciliation processes before positions are fully integrated into the cleared stack.

It is also important to contextualize that the use of large centralized crypto derivatives venues for delta-neutral carry strategies is a common industry pattern. Many institutional crypto yield products rely on venues such as Deribit and Binance for derivatives execution due to their liquidity and operational accessibility. From a risk perspective, the key diligence question is therefore not whether these venues are used, but whether their use is policy-bounded, monitored, and transparently disclosed.

To address this, the team intends to publish transparency reporting covering:

Current execution venues

Risk monitoring controls applied to each venue

Operational policies governing venue usage

The roadmap for CME integration as TVL scales

Treasury custody infrastructure is handled through Fireblocks, which manages operational wallet routing and asset custody.

From a structural perspective, the architecture is coherent with an institutional derivatives-based financing strategy. Clearinghouse involvement reduces bilateral default exposure; however, practical risk remains concentrated at the prime and FCM layers. The FCM in particular represents a central risk node because margin administration, legal segregation, collateral treatment, and insolvency mechanics are administered at that level. Institutional diligence should therefore focus less on the clearing venue label and more on account structure, margin utilization discipline, operational monitoring, and clearing relationship concentration.

1.3 Related-Party Arrangements

Fireblocks, FalconX, and Marex are independent third parties. No related-party treasury entities or affiliated custody structures are described in the execution stack.

2. Team and Key Roles

2.1 Founding Team

Jaron Abbott: former Head of Crypto Quant Research with Harvard mathematics training and CQF certification. Abbott's traditional finance background is substantial: CFA charterholder, pricing and risk infrastructure roles at Barclays and Citibank, algorithmic market-making at TransMarket Group, and Co-Head of Risk Analytics at Silver Point Capital.

Abbott's crypto track record requires disclosure. Abbott was listed as CRO at Tangible DAO in an Arbitrum Foundation grant application filed by re.al in March 2024. Tangible issued USDR, a stablecoin on Polygon backed primarily by tokenized UK real estate with a smaller liquid DAI reserve. On October 11, 2023, a redemption run drained all liquid reserves within hours, crashing USDR to approximately $0.50. The root cause was an asset-liability mismatch: on-demand redeemable tokens backed by illiquid property. A CoinDesk investigation published October 2024 separately revealed that Tangible's CEO had facilitated undisclosed related-party property transactions through a family member's company, with markups of up to 21% charged to the protocol treasury. Abbott was not a founder or CEO at Tangible, and no public evidence connects him to these transactions. Following the collapse, Tangible rebranded to re.al (Arbitrum Orbit L2) with the same core team. The grant application lists Abbott alongside CEO Jag Singh and four other Tangible personnel. re.al appears to have largely failed: its governance token lost approximately 99.9% of its value, and the USDR redemption process remains incomplete over two years later.

Abbott provided a written statement that we encourage readers to consult. He also provided us the following statement which includes comments on the above-mentioned Coindesk article:

Two years ago I did help out Tangible with some risk analytics work. USDR was already launched, and I was not involved in that design. But I did make many recommendations, as I mentioned in greater detail in my doc. To their credit, some of those mitigations were in progress, and might have helped, but the depeg happened first.

I think the Coindesk article had some valid critiques regarding transparency, but it also could have been better researched. For example, it's actually quite common, in real estate investing, for entities to negotiate bargains, and keep spreads as profit. And then if one entity gets used for initial purchases, in order to be able to snag it quickly, before the entity that's intended to actually hold it (at fair value) is even created, I mean... that to me is just being practical and efficient. And I see no reason why RICS is any less reputable for valuations than any other independent source (i.e. "UK professors"). Professionals will always quibble over these sorts of things. I did have valuation concerns, but that was more related to inclusion of tokenization costs into the value of each NFT.

Subsequent to that, I also managed Arcana, a tokenized risk-neutral strategy on re.al, earning consistent >20% for investors, and returned all capital plus profits when the chain shut down.

Today, I'm focused on Main Street, and looking after portfolio risk for the main box spread strategy, and I continue to independently do algo trading research.

Our Observations

There is some variance in how Abbott characterizes the role across contexts: "CRO" in the Arbitrum application (filed by re.al, not Abbott), "Head of Risk" in his written statement, and "some risk analytics work" in direct messages. We flag this without assuming intent. His technical account of the risks he identified is specific and credible. On the property markup scandal, it is plausible that a quantitative risk role would not have had visibility into property vendor selection, which falls under operations and executive leadership. Abbott's LinkedIn appears to have removed references to Tangible and re.al, though he has now addressed the history directly via the linked statement.

Xin Fan: quantitative developer with experience across CeFi and DeFi trading systems, holding an MS in Statistics from Michigan State University. Published ‘Extreme Value Prediction for Zero-Inflated Data’. PAKDD'12 Vol I, 318-329 and ‘Smoothed Quantile Regression for Statistical Downscaling of Extreme Events in Climate Modeling.’ CIDU, pp. 92- 106, (2011).

The technical orientation of the team is consistent with structured derivatives and systematic execution frameworks.

2.2 Governance Signers / Investment Committee

Governance authority resides in a Gnosis Safe multisig that controls upgrades, economic parameters, redemption settings, coverage ratio adjustments, and treasury deployment. Signer identities are disclosed only at a role level and unverifiable.

Given the findings in Section 2.1, the lack of publicly disclosed individual signer identities takes on additional significance.

Signer identities include according to the team executive leadership, trading and risk, engineering, and operations/finance, with optional independent participation. Signer identities are disclosed at the role level (Founder/CEO, Trading/Risk, Engineering, Operations/Finance, optional independent signer). The Owner multisig operates at a 3 / 4 threshold. Fee and distributor multisigs operate at 2 / 3 thresholds. Custodian Manager routing operates at 2/4 threshold. Individual identities are not publicly disclosed for security reasons, but thresholds, addresses, and role separation are publicly verifiable. Material decisions are described as passing through an Investment Committee-style internal process combining trading, engineering, and executive oversight. While centralized at present, the team describes DAO expansion and timelock introduction as potential future developments as the protocol matures.

There is no timelock currently implemented for upgrades or parameter changes. All such actions are auditable on-chain.

3. Product Overview and Architecture

3.1 Token Set

msUSD: functions as the accounting and redemption unit and is intended to be redeemable 1:1 for USDC subject to Coverage Ratio constraints.

smsUSD: represents a staked form of msUSD incorporating time-based exit mechanics.

msY: is structured as an ERC-4626 vault share representing exposure to the strategy’s net asset value.

3.2 System Design

On-chain contracts manage issuance, redemption, accounting logic, cooldown periods, coverage ratio enforcement, and administrative permissions. Off-chain systems manage portfolio construction, margin posting, hedge adjustments, roll management, and liquidity coordination.

This separation reduces smart contract complexity but introduces operational and counterparty risk concentration.

4. Strategy: CME Index Options Box Spreads

4.1 Mandate

Historically, leverage has remained within a controlled operational band. The strategy operates with a target leverage range of approximately 2x to 4x, with an explicit hard cap of 4.25x leverage defined as an internal policy limit.

Leverage may fluctuate within this band due to several structural factors inherent to derivatives trading. These include changes in venue margin parameters during volatility regime shifts, changes in assets under management resulting from inflows or redemptions, and temporary margin utilization adjustments during roll or unwind windows.

To improve curator verification and transparency, the team has indicated that they intend to publish standardized leverage metrics that allow external monitoring without revealing proprietary trading details such as strike prices or expiration dates. These disclosures are expected to include a maximum leverage watermark and monthly leverage distribution statistics (p50, p90, and maximum values).

The key underwriting point is that leverage changes are policy-bounded and driven by margin regime mechanics rather than discretionary risk-taking.

Yield accrues through appreciation in ERC-4626 share value rather than periodic distribution.

4.2 Box Spread Mechanics (conceptual)

A box spread consists of a call spread and put spread constructed with identical strike differentials and expiration dates. When priced efficiently, the payoff at expiration is deterministic and reflects an implied financing rate embedded in options markets.

While theoretically neutral at expiration, interim mark-to-market exposure and margin requirements introduce path dependency risk. Convexity exposure arises particularly when the structure includes short-gamma components requiring dynamic hedging.

4.3 Strategy Drift Controls

Any material deviation from the mandate would require announcement and updated disclosures. The teal describe constraints as: (i) governance constraints (Owner multisig controls upgrades/parameters, with internal policy + governance approvals for material changes), (ii) operational constraints (regulated-market execution stack is specialized; not a generic vault for arbitrary deployment), and (iii) disclosure constraints (mandate changes reflected in docs/risk materials/comms).

5. Off-Chain Execution, Counterparty, and Margin Risk

5.1 Clearing and Segregation

MainStreet’s core execution stack is described as CME index options execution routed through FalconX, with clearing performed by Marex as the FCM. This establishes the protocol’s primary off-chain risk concentration: while on-chain contracts can enforce accounting and redemption logic, the economic integrity of the strategy depends on how positions are margined, cleared, and protected under the applicable customer protection regime.

Marex, acting as FCM, is subject to CFTC customer protection and segregation regimes, including Rule 1.20 frameworks for cleared CME positions. CME-cleared futures and options are margined and held within the FCM clearing stack in accordance with applicable customer fund protections. Collateral consists of cash and T-bills. Marex publishes daily segregation reporting, providing transparency into regulatory capital and customer fund treatment. The clearing structure is FalconX → Marex → CME. In practice, this distinction matters because the insolvency waterfall, portability of positions, treatment of excess margin, and timing of customer fund distributions depend on account type and documentation, not merely on the venue’s general reputation or the fact that it is regulated. The clearing arrangement is currently concentrated through the FalconX → Marex path, with diversification across clearing relationships described as a roadmap item rather than an implemented safeguard.

5.2 Insolvency and Concentration

The critical counterparty concentration is that the system’s trading and margin operations depend on a small number of entities: FalconX as prime/execution layer and Marex as the clearing member. If the FCM were to become insolvent or experience operational disruption, outcomes would be shaped by (i) the account type and legal agreements, (ii) the operational ability to port or close positions, and (iii) the speed at which collateral and positions can be mobilized. The team describes maintaining buffers, continuous monitoring, and the ability to halt execution or reduce risk under stress conditions.

Because the strategy is implemented through cleared derivatives, there is an intuitive tendency to over-assume safety by proxy of “regulated clearing.” The correct framing is narrower: clearing reduces bilateral counterparty risk to specific cleared regimes, but does not eliminate operational dependency on the FCM and prime stack, nor does it remove liquidity and margin path-dependency during sharp volatility. The team’s stated mitigation direction is to expand clearing relationships over time, but the current state remains concentrated.

5.3 Margin Assets and Utilization

The team indicates that margin collateral consists of both cash and Treasury bills, consistent with the types of collateral typically accepted within institutional prime brokerage and clearing structures.

Maximum observed margin utilization has historically remained within the leverage limits described by the team. Rather than relying solely on internal disclosure, the team has indicated that they intend to publish curator-verifiable leverage monitoring metrics that allow external stakeholders to independently observe leverage behavior over time without exposing proprietary position details.

These disclosures are expected to include:

maximum leverage watermark since launch

monthly leverage distribution statistics (p50, p90, and maximum)

high-level margin utilization summaries

Intraday monitoring is described as automated and high-frequency, using venue-sourced marks and account state reconciliation. Monitoring covers margin utilization, Coverage Ratio dynamics, and collateral buffers.

De-risking triggers include buffer breaches, abnormal volatility regimes, data anomalies, and roll window concentration risk. These triggers are conceptually appropriate for a derivatives-based financing strategy because risk typically manifests through a combination of mark-to-market variance, margin call dynamics, and liquidity conditions during hedge adjustments or roll transitions.

The material diligence question therefore remains not only whether monitoring exists, but whether monitoring thresholds and leverage discipline remain conservative relative to volatility stress environments and redemption dynamics.

6. NAV, Valuation, and Proof-of-Solvency

6.1 NAV Formula

msY is an ERC-4626 vault where NAV per share is computed as totalAssets divided by totalSupply. In this framework, unrealized PnL is included mark-to-market using venue marks, and variation margin effects are reflected through cash and receivable movements as reported by clearing and venue statements. Fees accrue according to protocol parameters and are reflected through the vault’s accounting mechanics rather than discretionary off-chain adjustments.

This design choice is structurally coherent: it aligns user-facing share value with observable portfolio marks rather than smoothing or model-based valuation. However, it also implies that users are directly exposed to the mark-to-market path of derivatives positions even if the end payoff profile is “deterministic at expiry.” For due diligence, that means that liquidity and redemption design must be evaluated alongside NAV mechanics, because NAV volatility can translate into Coverage Ratio dynamics.

6.2 Marking Methodology and Update Frequency

Marking methodology is stated as purely venue-sourced: CME marks for CME positions, FalconX marks for the CME-facing account context, and Deribit marks for Deribit positions where used. The team states they do not apply proprietary marking models. NAV and reserves reporting operate at high frequency, with a target attestation cadence of approximately fifteen minutes. Marking is venue-sourced (CME, FalconX, Deribit) with no proprietary valuation models applied. Inputs are fetched via API and reconciled internally through the Accountable integration pipeline.

The key diligence point is that high-frequency marking improves transparency and reduces the risk of stale reporting, but it increases reliance on API availability, reconciliation correctness, and incident response procedures for feed anomalies. It also means that any temporary dislocation in marks during stress can be reflected quickly and visibly, which is positive for transparency but can amplify redemption pressure if users react reflexively.

6.3 Validation, Downtime, and Safety Controls

NAV inputs are fetched via API by Accountable and reconciled internally. The team indicates independent review or attestation may be added as the protocol scales. They also describe operational controls for downtime or data anomalies, including potential publication of a last-known-good NAV timestamp and application of safety controls during incident response events.

For institutional evaluation, the most important question is whether “safety controls” are strictly bounded, pre-communicated, and consistent with redemption fairness, because any discretion applied during NAV uncertainty can be perceived as governance risk. The team’s broader disclosures imply an intent to prefer conservative halts and last-known-good reporting rather than discretionary re-marking.

6.4 Dashboard Architecture and Coverage Ratio Representation

The protocol dashboard displays NAV per share, total assets, total liabilities, and Coverage Ratio (CR). Coverage Ratio is generally defined as total backing assets divided by outstanding msUSD liabilities.

NAV is computed using venue-sourced marks (CME, FalconX, Deribit where applicable) and reflected in ERC-4626 accounting via totalAssets / totalSupply. Mark-to-market PnL is incorporated through variation margin movements and unrealized mark updates.

The dashboard figures are derived from API-sourced data feeds reconciled internally through the Accountable integration pipeline. The stated target update cadence is approximately fifteen minutes.

It is critical to distinguish between on-chain observable balances and off-chain cleared collateral. NAV includes mark-to-market valuation of derivative positions and cash equivalents, but certain buffers (such as insurance fund holdings) may not be directly included in the displayed CR depending on accounting treatment.

For institutional diligence, the key requirement is understanding precisely:

What assets are included in NAV.

Whether unrealized PnL is fully reflected.

Whether insurance balances are included or excluded.

How frequently feeds are reconciled.

What occurs if API feeds fail or marks are stale.

Clarity on these mechanics determines whether CR is a conservative solvency indicator or a narrow accounting ratio.

6.5 Oracle Infrastructure

MainStreet uses RedStone Oracle to publish the fundamental price feeds for msY and msUSD on Ethereum.

These feeds provide standardized on-chain pricing references used by integrations and external protocols, rather than relying on custom protocol-specific price calculations.

Relevant feeds include:

Using an external oracle provider reduces reliance on custom pricing infrastructure and enables transparent, independently verifiable price data for on-chain integrations.

7. On-Chain Contracts, Upgradeability, and Permissions

7.1 Upgradeability Model

No timelock is currently used for upgrades and that there is no modification history under such a timelock framework.

From a risk perspective, the absence of a timelock increases the protocol’s dependence on multisig operational integrity and signer discipline. It also increases the importance of role separation, internal change control, and the importance of clearly disclosed threshold structures, role separation, and publicly verifiable Safe addresses. Individual signer identities are intentionally withheld for security reasons, but governance thresholds and functional segregation are transparent. The appropriate diligence posture is not to assume malicious intent, but to explicitly account for the fact that upgrade risk is a live governance risk surface today.

7.2 Admin / Control Surface

There is a broad set of owner/admin functions that can affect protocol economics and safety, including vault controls and minter controls such as fee and tax settings, rewarder and fee routing configuration, coverage ratio settings, cooldown management, deposit toggles, supported asset management, oracle staleness parameters, redemption enable/disable toggles, and redemption cap configuration.

This breadth is not unusual for a protocol in a pre-DAO stage where operational responsiveness is treated as a requirement. The diligence requirement is to understand how these controls are constrained by internal policy and what is communicated publicly when changes occur. The team indicates that parameter changes are auditable via on-chain transactions and emitted events where implemented, and that governance actions are auditable on-chain via emitted events and transaction history. Material changes are communicated through documentation updates and transparency reporting.

7.3 Key On-Chain Addresses

Role / Contract | Address |

Owner (protocol admin / upgrades / key parameters) - Gnosis Safe | 0x0eAe4ACb10f3e5696cF6B0de33693eF8EC571858 |

Fee Silo contract | 0x6665efDe9f1916a9e16f7f955375ecD392b98B81 |

Distributor / Fee collection multisig | 0xB72Db4E3bDf013b6386e3e17a5a999230A9a7F98 |

Custodian Manager contract | 0x4cC94169605069DDf82C815493Cf6048f1935D0A |

8. Liquidity, Redemption Mechanics, and Stress Scenarios

8.1 Redemption Flow

The redemption process is multi-step and can involve position unwinding and operational asset conversion, with USDC received after a cooldown. On-chain, the minter uses a two-step request/claim flow where the request burns msUSD and creates a time-delayed claim, and the claim transfers collateral subject to caps and coverage ratio logic.

The redemption process is structured as a staged liquidity mechanism rather than an instantaneous 1:1 swap facility. On-chain, redemptions follow a request/claim architecture in which a user initiates a redemption request, the corresponding msUSD is burned, and a time-delayed claim is created. Following the cooldown period and subject to system parameters, the claim can be executed for USDC, contingent on Coverage Ratio (CR) constraints and redemption caps.

This structure reflects the economic reality of the underlying strategy. MainStreet’s assets are deployed in CME-cleared derivatives positions that require margin posting and follow expiry and roll mechanics. As a result, liquidity availability depends on unencumbered collateral, margin buffers, and the timing of derivative settlement cycles. “1:1 redeemable” should therefore be interpreted operationally rather than mechanically instantaneous.

A critical dimension of redemption analysis concerns drawdown periods. While box spreads are theoretically deterministic at expiry, interim mark-to-market drawdowns can occur due to volatility shifts, liquidity dislocations, rate repricing, or convexity exposure. During such periods, NAV may decline and CR may fall below 100%, even if the strategy is expected to converge at expiry.

Redemption behavior under drawdown conditions is structurally important. If redemptions are processed at par while CR is impaired, early redeemers could extract disproportionate value, leaving remaining participants with crystallized losses. To mitigate this asymmetry, the team has indicated an intent to process redemptions at the prevailing CR when CR < 100%, thereby enforcing pro-rata loss realization and reducing bank-run incentives.

In a bank-run scenario during a drawdown, system resilience depends on three interacting variables:

First, margin sufficiency. If margin buffers are conservatively maintained, positions can remain open through volatility until expiry, allowing deterministic payoff mechanics to restore CR without forced liquidation.

Second, liquidity sequencing. If redemption demand exceeds available unencumbered collateral, the system may need to unwind positions prior to expiry. The speed and cost of this unwind depend on market depth, volatility regime, and hedge positioning.

Third, liquidation risk. If mark-to-market losses breach margin thresholds before orderly unwind is possible, forced position reduction may occur at adverse prices, crystallizing losses rather than allowing convergence to expiry value.

To address these risks, the protocol incorporates multiple stabilizers: redemption cooldowns, caps on redemption processing, insurance fund support, and governance-controlled safeguards. During the October 2025 volatility episode, temporary measures were implemented to extend redemption windows and reduce forced execution risk, illustrating that redemption design functions as a systemic stabilizer rather than a pure convenience feature.

It is important to clarify that the October 2025 volatility event referenced relates to a separate legacy product and not to the msUSD/msY box-spread system evaluated in this due diligence report. As such, the event should be interpreted as historical operational context rather than a performance event within the current strategy.

From an institutional diligence perspective, the key evaluation points are:

Whether margin utilization bands are sufficiently conservative relative to historical volatility stress envelopes.

Whether redemption pricing is mechanically aligned with CR rather than discretionary governance decisions.

Whether insurance deployment rules are pre-defined and transparently disclosed.

Whether unwind sequencing under stress has been scenario-modeled and documented.

For a derivatives-based financing protocol, solvency risk is path-dependent rather than expiry-dependent. Redemption architecture therefore becomes a primary determinant of stability under stress. The system’s resilience depends not on theoretical payoff determinism at expiry, but on the interaction between margin discipline, CR transparency, and orderly redemption sequencing during volatility shocks.

8.2 Stress Modeling

The team highlights that in a scenario involving a large fraction of TVL redeeming within a short window during a significant rate shock, strategy positions with short-dated expiries may constrain capital return by expiry timing. Under such conditions, concentrated redemption demand may need to wait for expiries rather than forcing pre-expiry liquidation at unfavorable marks.

Operational response tools described include maintaining margin buffers, staggering roll schedules, and allowing positions to mature when possible rather than forcing liquidation.

The current system’s risk framework therefore focuses on managing redemption pressure and margin dynamics without assuming that past events from unrelated strategies apply directly to the present architecture.

There are 3 ways to mitigate a bank run built into the msY contracts in case CR drops beneath 100%. If this is just a temporary m2m drop and it will return:

1) setCooldownDuration to Increase the redemption cooldown period to allow for the m2m loss to recover.

If the loss was permanent for some reason like a failing of an FCM or some force majeure then there is 2 additional steps already built into the contracts to prevent there being a rush to the exits and ensure everyone is treated fairly even those who rush to cooldown before we can take action:

2) burnAsset to burn msUSD inside the msY vault to correspond to the current CR this sets the CR of the vault to match the NAV and is applied to everyone:

3) setCoverageRatio is for users that submitted an exit before we could do the above. When they exit, coverage ratio will be applied to them (they exit when their cooldown expires)

The charts model how two different redemption mechanisms behave when the Coverage Ratio (CR, ratio of total backing assets to outstanding msUSD liabilities) falls below 100%. The left panel shows how CR evolves for remaining holders as an increasing fraction of the total msUSD supply exits the protocol. The right panel shows the effective recovery rate, how many USDC cents a redeemer receives per msUSD, depending on how early or late they exit relative to others. Under a par redemption mechanism (solid lines), each redeemer receives 1 USDC per msUSD regardless of the current CR. This creates a structural first-mover advantage: early redeemers are made whole at the expense of those who exit later. CR collapses progressively for remaining holders with each redemption processed at par.

The right panel illustrates the binary outcome: redeemers who exit before assets are exhausted receive 100%, while those who exit after receive zero. At CR₀ = 90%, assets run out after 90% of the supply has redeemed, the last 10% of holders are wiped out entirely. This dynamic incentivizes every rational participant to exit as fast as possible the moment CR drops below 100%, creating a self-reinforcing bank-run mechanic. Under an at-CR redemption mechanism (dashed lines), each redeemer receives CR USDC per msUSD, the prevailing coverage ratio at the time of exit. As shown analytically, this keeps CR perfectly flat for remaining holders regardless of how many people redeem. Every participant shares the loss pro-rata, and no advantage accrues from exiting early. The bank-run incentive is eliminated by design. As of the writing of this report, MainStreet's redemption contracts have not yet implemented the at-CR mechanism as deterministic on-chain logic. The team has stated the intent to upgrade the contracts accordingly. Until this upgrade is live, the bank-run incentive structure illustrated in the left panel remains a live risk surface during any under-coverage episode, as partially evidenced by the October 2025 stress event, during which the team activated temporary safeguards precisely to manage this dynamic.

Note: this October 2025 event relates to a discontinued legacy product, not the current msUSD/msY box-spread system; it is referenced only as historical context illustrating the team’s response to market stress.

8.3 Under-Coverage Handling

The team states that design intent is equal treatment and no preferential ordering. Under coverage shortfall, the preferred approach is a pro-rata haircut mechanism to avoid bank-run incentives. Redemption controls such as caps and enable/disable switches exist, and the team states that gating had not been activated historically prior to the October 2025 safeguard activation.

For diligence, the critical feature is whether under-coverage handling is implemented as deterministic on-chain logic rather than discretionary governance. The team’s described plan to process redemptions at the prevailing CR when CR is below 100% would move the system in a more deterministic direction.

9. Insurance Fund and Coverage Ratio

9.1 Composition and Addresses

The team states that the insurance fund is currently held in msUSD and is not included in the NAV or coverage ratio displayed on the dashboard today. Holding msUSD functions economically as a loss absorption buffer because burning msUSD increases the remaining backing per unit.

This construction simplifies custody and accounting but introduces communication complexity: external observers may underestimate total economic backstop capacity if they rely strictly on the displayed Coverage Ratio.

To improve transparency and clarify expectations around insurance usage, the team has proposed a structured insurance deployment policy.

Coverage is defined as the ratio between assets attributable to msUSD backing and outstanding redemption liabilities, using venue-sourced marks (currently Deribit and Binance marks).

Proposed deployment policy:

Soft trigger (monitor and de-risk): If coverage falls below 99.75% for more than 24 hours, the team publishes an incident note and begins de-risking actions such as reducing gross exposure, increasing buffers, or allowing positions to mature until coverage normalizes.

Hard trigger (insurance deployment): If coverage falls below 99.50%, or if a realized shortfall emerges due to unwind costs, the insurance fund may be deployed to restore full coverage.

Daily deployment limits may be applied when losses are unrealized in order to avoid reacting excessively to temporary mark-to-market dislocations.

Disclosure policy

Any insurance deployment would be publicly disclosed within 24 hours, including the size of the deployment, the cause of the shortfall, the resulting coverage level, and follow-up remediation actions.

This framework maintains governance discretion while reducing ambiguity about when and why the insurance buffer would be used.

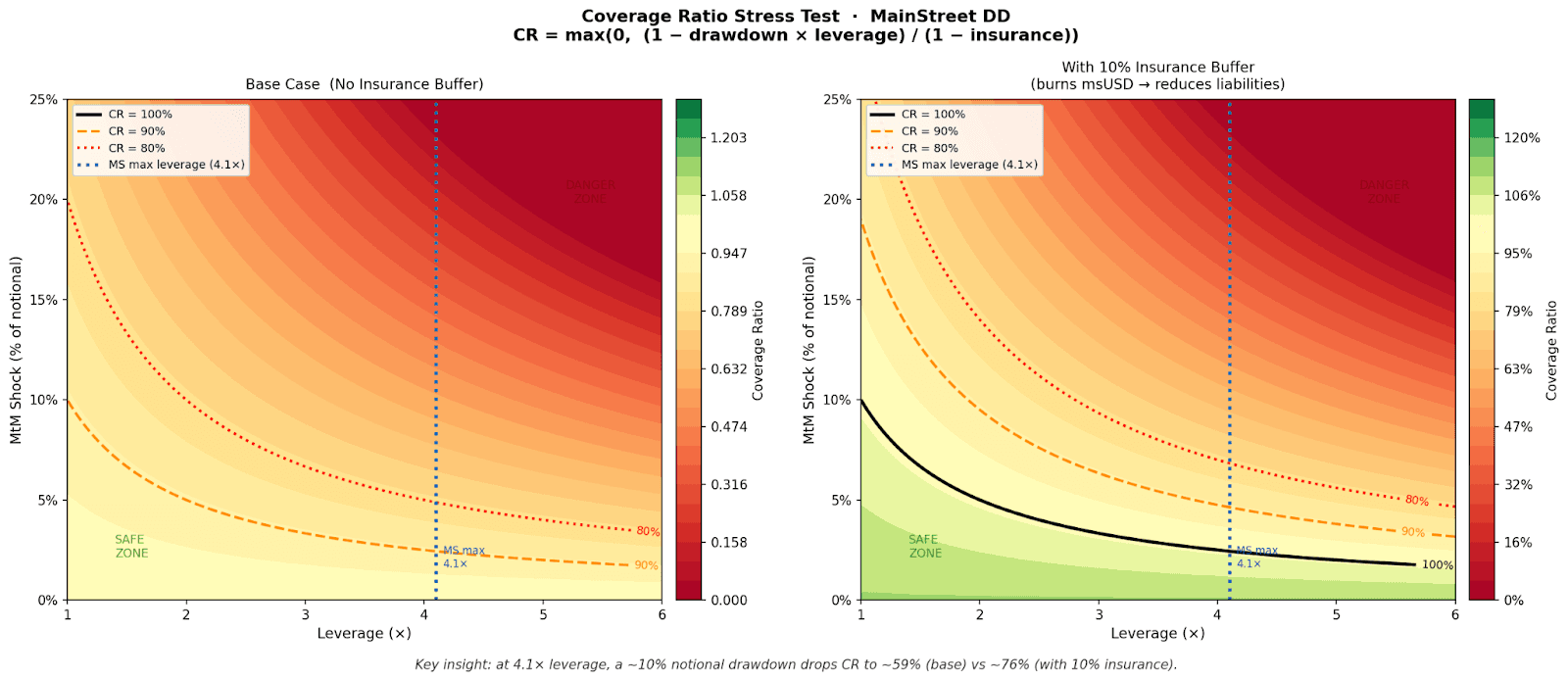

The charts show how MainStreet's Coverage Ratio (CR, the ratio of total backing assets to outstanding msUSD liabilities) responds to two variables: the level of leverage deployed and the magnitude of a mark-to-market (MtM, the real-time revaluation of open positions at current market prices) loss on the derivatives portfolio. How to read the chart. Each point on the map corresponds to a combination of leverage (X axis) and MtM shock (Y axis). The color indicates the resulting CR: green means full coverage, red means impairment. The dashed lines mark the CR = 100%, 90%, and 80% thresholds. The vertical blue line indicates MainStreet's disclosed maximum leverage (4.1×). The key takeaway. At 4.1× leverage, a MtM loss of just 2.4% on the notional is sufficient to push CR below 100%, i.e., into under-collateralization territory. A 10% loss brings CR down to approximately 59%. This does not necessarily imply a permanent loss: box spread positions converge to a deterministic payoff at expiry. However, during the life of the trade, if the MtM drawdown is large enough, the protocol may find itself in a position where redemption demand exceeds available unencumbered collateral, as demonstrated by the October 2025 episode.

Note: this October 2025 event relates to a discontinued legacy product, not the current msUSD/msY box-spread system; it is referenced only as historical context illustrating the team’s response to market stress.

The role of the insurance fund. The right panel shows the effect of a 10% insurance buffer (held in msUSD, MainStreet's USD-denominated token). Burning msUSD reduces outstanding liabilities, which is economically equivalent to lifting CR. With this buffer, the same 10% loss brings CR to approximately 76% rather than 59%, a materially wider margin before reaching critical thresholds. The gap between the two panels therefore quantifies the real value of the insurance fund, which MainStreet's dashboard currently excludes from the displayed CR figure.

9.2 Deployment and Governance

Insurance fund deployment is discretionary via governance/multisig controls. It is intended to backstop shortfalls and support orderly redemptions or absorb stress unwind costs, including temporary mark-to-market dislocations during rate shocks. Treasury withdrawal or reallocation is possible under governance controls and internal policy, with the team stating it would be disclosed via transparency reporting.

Given the discretionary nature, the primary diligence issue is governance integrity and disclosure discipline rather than mechanical eligibility. nsurance fund deployment is discretionary via governance/multisig controls and is intended to backstop shortfalls, stress unwind costs, or support orderly redemptions. The insurance balance and relevant Safe addresses are publicly disclosed. Movements are subject to internal policy and transparency reporting.

10. Governance and Operational Readiness

10.1 Parameter Changes and Timelocks

The team states that non-upgrade parameter changes, including fees, redemption caps, and coverage ratio parameters, are not currently timelocked. The reason provided is that the protocol is in a pre-DAO stage and requires operational responsiveness. They indicate that timelocks and broader DAO governance may be introduced as the protocol matures.

This implies that the short-term trust model is multisig-centric. The correct diligence framing is therefore to evaluate the controls around multisig decision-making, internal approvals, monitoring, and the transparency with which parameter changes are communicated.

10.2 Reporting and Transparency

Monthly performance reviews and reports, alongside ongoing dashboard monitoring and proof-of-solvency tooling. The team plans to publish structured transparency reporting including gross yield, leverage cost, fees, and realized slippage at a summary level, while withholding position-level strike, venue, and duration details to preserve competitive execution integrity.

The October 2025 episode, in particular, indicates that the team is willing to publish structured incident updates, define checkpoints, and propose governance mechanisms to resolve fairness concerns when CR is below 100%.

11. Compliance and Legal Recourse

11.1 Restricted Jurisdictions

US persons are restricted from minting and redeeming. The team indicates additional restricted jurisdictions, including sanctioned jurisdictions, are restricted under compliance policy.

11.2 Insolvency Rights and Disputes

Tokenholder economic rights are described through token mechanics. msY represents an ERC-4626 share of vault assets; msUSD is a claim on backing as described by the protocol’s redemption and coverage framework. Creditor status and legal recourse depend on governing terms and jurisdiction. Dispute jurisdiction is stated as BVI.

The team indicates there is no formal legal opinion letter currently classifying msUSD/msY, but they state confidence it is not a security and would obtain a legal opinion if required for listings.

12. Operational Risk and Incident Management

12.1 Incident Response

The team states a documented incident response plan exists covering NAV and marking anomalies, counterparty/connectivity incidents, smart contract incidents, and liquidity or redemption stress events. Communications include public updates and post-mortems where appropriate.

The October 2025 volatility episode is consistent with this posture and provides a concrete example of public communication and temporary safeguard activation.

12.2 Alerts and De-Risking

Monitoring is ongoing and includes automated tracking of:

margin utilization

Coverage Ratio thresholds

venue mark reconciliation

oracle and data feed staleness

liquidity and redemption capacity

insurance fund balance

Monitoring relies primarily on venue marking engines and account state reconciliation, currently sourced from Deribit and Binance and expected to include CME marks once CME integration is operational.

Institutional-grade controls are implemented through predefined monitoring thresholds and structured escalation procedures.

These include:

Policy-bound monitoring thresholds

Margin utilization bands and coverage bands are defined internally with associated response actions. These bands typically correspond to normal operation, monitoring states, and incident states where risk reduction actions are triggered.

Alert escalation

Automated alerts feed into an incident escalation matrix with defined severity levels and on-call response procedures. Operational authority exists to halt new exposure and rapidly reduce risk if thresholds are breached.

Redundancy

Monitoring infrastructure uses multiple data sources including venue APIs and broker reporting where applicable, supported by manual override procedures in case of feed disruptions.

Transparency roadmap

As the protocol scales, the team plans to publish a transparency report including:

leverage watermark statistics

coverage ratio monitoring metrics

insurance fund balance

high-level venue usage summaries

The protocol does not currently enforce a strict venue concentration limit, but the team has indicated that venue diversification policies may be introduced as TVL grows in order to reduce concentration risk.

13. Security, Audits, and Monitoring

Two WatchPug audits with no critical or high severity issues in summaries, plus a bug bounty program described as forthcoming. Expanded monitoring is described as ongoing.

WatchPug Security Audit 1: Completed July 18, 2025; scope described as “Mainstreet v2 smart contract system”; summary states 11 total issues (1 medium, 4 low, 6 informational/code quality), no critical/high, with 4 fixed and 7 acknowledged.

WatchPug Security Audit 2: Completed Dec 18, 2025; scope described as “Mainstreet StakedmsUSD & msYBridger smart contract system”; summary states 6 total issues (1 medium, 3 low, 2 informational/acknowledged), no critical/high, with several items fixed or acknowledged by the team.

14. Market Risk - Liquidity

14.1 Empirical depth (aggregator results)

Small trades (< $10k): near 1:1, negligible slippage (Paraswap routing).

Mid trades (~$10k–$100k): small slippage; mostly absorbed across Uniswap v3 + Balancer v3.

Mid-large (~$250k–$500k): slippage accelerates and imbalance appears.

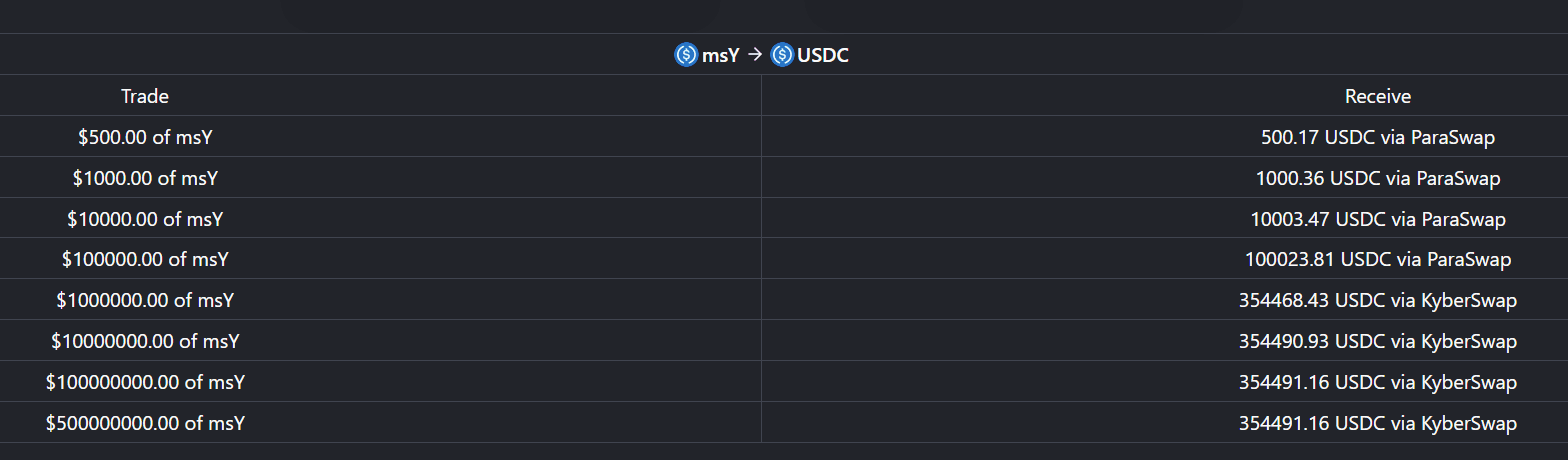

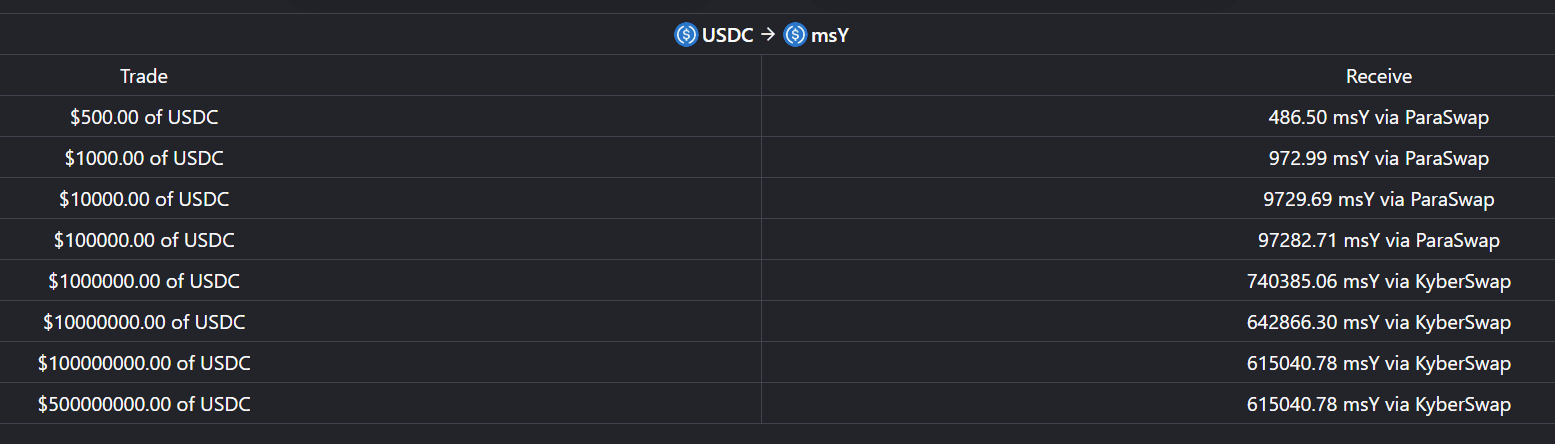

Large (> $1M): effective execution plateaus, selling $1M of msY returned ~$354k USDC in your snapshot; additional size beyond that did not materially increase received USDC (clear sign of depth exhaustion).

Immediate usable single-ticket exit capacity is empirically ≈ $300k–$400k USDC before the market stops clearing proportionally.

Source: DeFiLlama Empirical depth

14.2 Liquidity Venue Concentration

Here are the top liquidity venues by TVL (as of March 02, 2026):

Uniswap v3 pool: concentrated liquidity pair (0.99005-1.01) at 0.05% fee, on-chain address provided (0xd3c235…c635c). Liquidity depends on tick placement.

$479k TVL, 72% msUSD - 28% msY

concentrated liquidity provides excellent near-spot execution while LP ranges are active. If LPs concentrate around current price, depth for larger orders is thin outside those ticks.

Balancer v3 stable pool: AMP = 5,000, swap fee = 0.01% (governance editable), LP token price ≈ $1.01 (creation 17 Dec 2025). Pool behaves like a high-A StableSwap curve: very flat around peg; steep tails once imbalance grows.

$984k TVL, 36% msUSD - 64% msY

wide flat region around 1:1, excellent for small to moderate trades while pool remains balanced. But once directional flow creates imbalance, the invariant steepens quickly → convex slippage. High A reduces slippage near peg but does not add absolute capital. Result: a liquidity cliff once imbalance crosses the flat band.

14.3 Exchanges

msY is exclusively traded on DEXs and is not currently listed on any centralized exchange.

14.4 Volatility

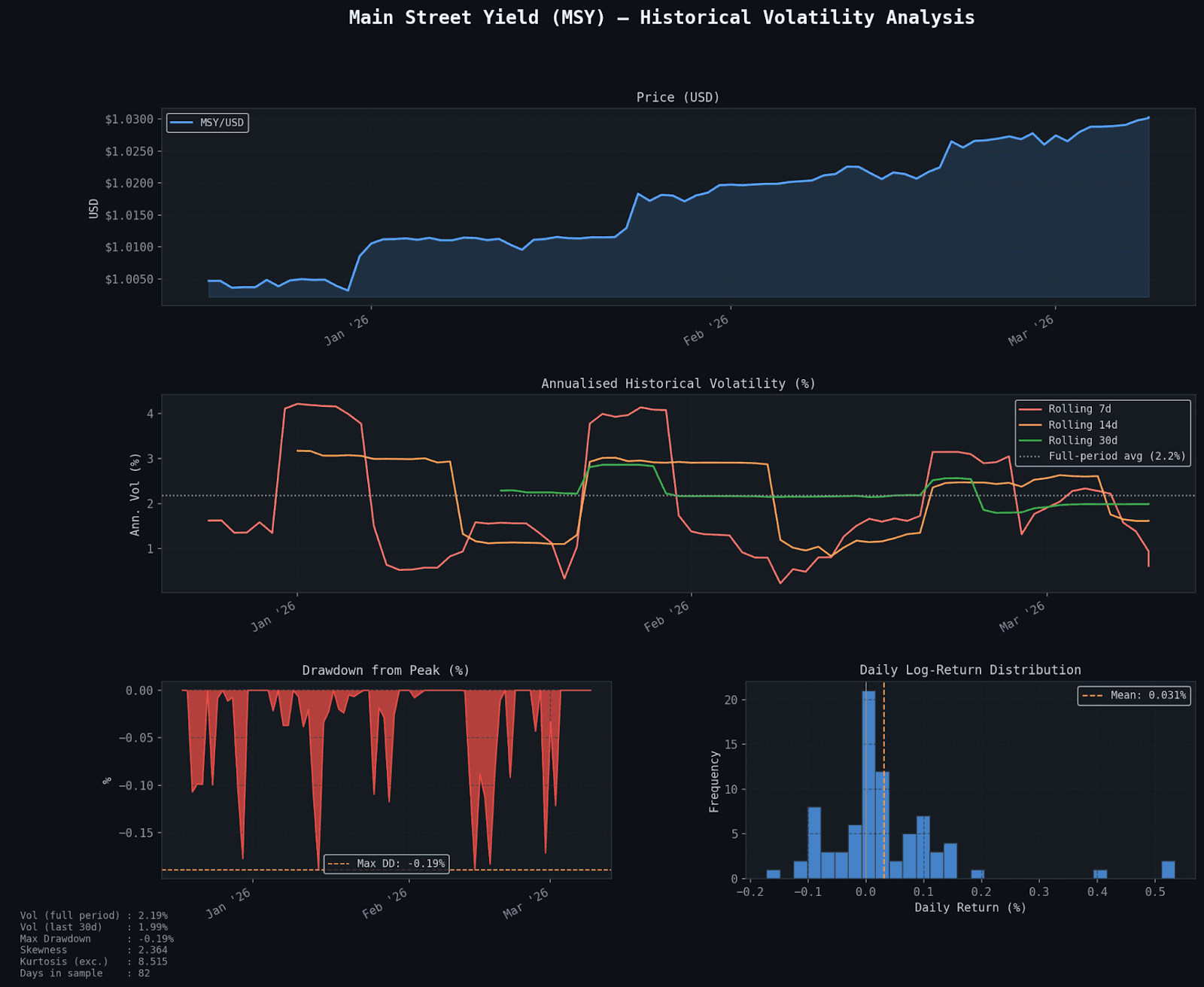

Historical price behavior for msY indicates a very low realized volatility profile relative to typical crypto assets, consistent with the characteristics expected from a derivatives-based financing strategy.

Over the observed period (~82 trading days), the msY price exhibits a gradual and largely monotonic appreciation pattern. The price increased from approximately $1.004 to $1.030, representing roughly ~2.6% cumulative appreciation during the sample window. Price movements appear smooth with limited short-term drawdowns, reflecting the carry-like nature of the underlying box spread strategy.

Empirical volatility metrics derived from the dataset show:

Annualized historical volatility (full period): ~2.19%

Rolling 30-day volatility: approximately ~2.0%–2.3%

Rolling 14-day volatility: approximately ~2.5%–3.0%

Rolling 7-day volatility peaks: up to ~4%

For context, this volatility level is significantly lower than most crypto-native assets and even lower than many traditional risk assets. Such behavior is consistent with strategies designed to capture implied financing spreads rather than directional market exposure.

Drawdown analysis further reinforces the stability profile. The maximum observed drawdown over the sample period is approximately −0.19%, indicating limited short-term NAV deviations during the observation window.

Daily return distribution analysis provides additional insight into the statistical properties of the strategy:

Average daily return: ~0.031%

Implied annualized return: ~11%

Skewness: positive (~2.36)

Kurtosis: elevated (~8.5)

Positive skewness suggests a return distribution characterized by frequent small gains with occasional larger positive observations. Elevated kurtosis indicates heavier tails than a normal distribution, meaning extreme observations remain possible despite the generally stable return profile.

From a risk perspective, it is important to interpret these statistics correctly. Low realized volatility does not necessarily imply the absence of risk. In derivatives-based carry strategies, risk is often event-driven rather than continuously distributed. Potential stress vectors include:

sudden volatility regime shifts affecting margin requirements

liquidity disruptions during roll or unwind windows

counterparty or clearing layer disruptions

large mark-to-market swings prior to expiry convergence

As a result, the primary risk dimension is path dependency during stress events, particularly when leverage and margin requirements interact with redemption demand and liquidity constraints.

Overall, the empirical volatility profile of msY aligns with expectations for a structured financing strategy built on CME index options box spreads: low realized volatility, steady carry-driven appreciation, and limited historical drawdowns, with risk concentrated in rare but potentially impactful stress scenarios rather than in day-to-day price fluctuations.

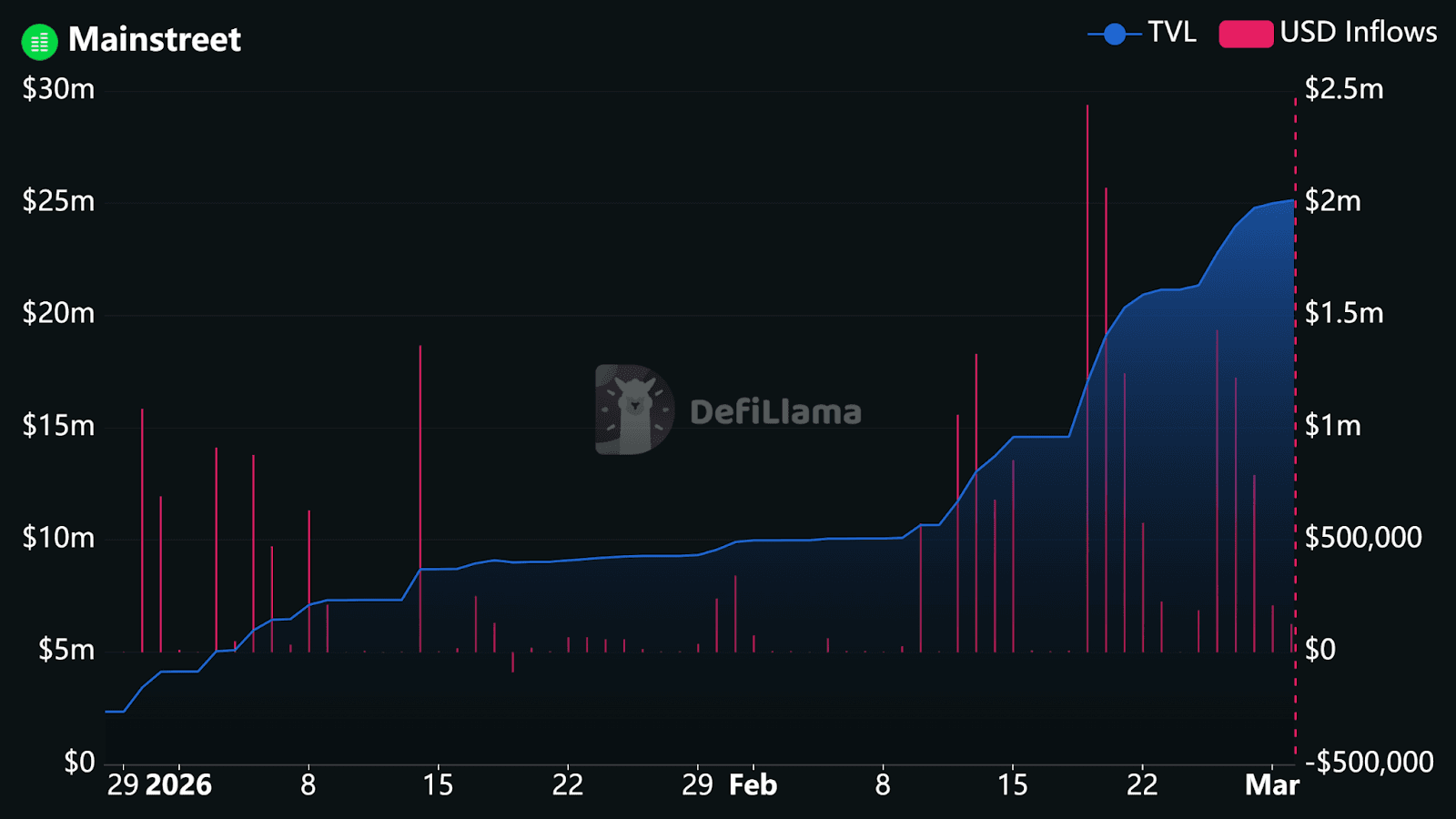

14.5 Growth

msY has experienced material growth in total supply and reserves over the observed period (mid-January to early March).

Total Supply increased from approximately $7–8M in mid-January to approximately $22M+ by early March.

Total Protocol Reserves increased to $25.19M.

Current reported Collateral Ratio: 100.28%.

Net overcollateralization: +0.28%.

The growth pattern is stepwise rather than linear, indicating:

Discrete capital inflows (large deposits)

Likely coordinated treasury or partner allocations

Non-retail dominant expansion

This reflects a >3x increase in TVL within ~6 weeks, which is structurally meaningful relative to the starting base.

14.6 Inflow Dynamics

USD inflow bars show:

Intermittent large inflow spikes (>$1M days)

Periods of near-flat net flow

No sustained multi-week outflow regime

Growth appears episodic, driven by concentrated deposits rather than organic daily demand.

This concentration dynamic introduces two considerations:

Growth sustainability depends on a limited number of capital allocators.

Reversal risk increases if those same allocators unwind positions.

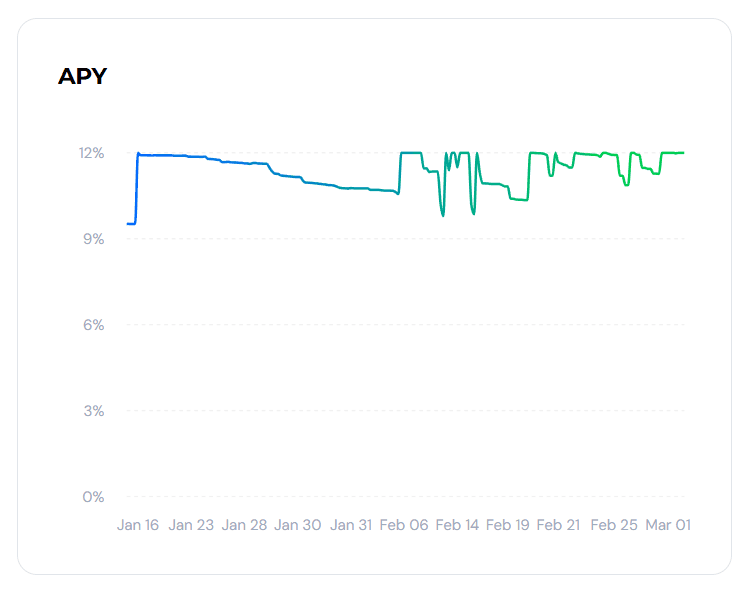

14.7 Yield Stability as Growth Driver

APY has remained relatively stable:

~9.5%–12% range

Recent stabilization near ~12%

Stable yield in the 10–12% range likely acts as the primary growth attractor.

Conclusion

MainStreet represents a structurally interesting attempt to bring institutional derivatives financing strategies on-chain through a tokenized vault architecture. By packaging CME index options box spreads into an ERC-4626 structure, the protocol provides DeFi users access to implied financing rates traditionally available only through prime brokerage and clearing relationships.

From a structural standpoint, the architecture is coherent. The separation between on-chain accounting and off-chain execution reduces smart contract complexity while allowing the strategy to operate through regulated derivatives infrastructure. However, this design also introduces operational dependencies on the execution stack, particularly the FalconX prime layer and Marex clearing relationship, which remain key diligence considerations.

The strategy itself is conceptually market-neutral at expiry, but the system remains exposed to interim mark-to-market volatility, margin dynamics, and liquidity constraints inherent to derivatives portfolios. As a result, solvency risk is path-dependent rather than purely expiry-dependent. The protocol’s Coverage Ratio framework, insurance buffer, and staged redemption mechanics are designed to mitigate these dynamics, though their effectiveness ultimately depends on conservative leverage discipline, transparent monitoring, and predictable governance responses during stress periods.

Governance currently relies on a multisig model without timelocks, reflecting an early operational stage. While this structure allows rapid response to market events, it also places greater emphasis on transparency, disclosure discipline, and internal risk controls until more decentralized governance mechanisms are introduced.

Market traction has been notable, with TVL increasing materially over a short time frame and yields remaining relatively stable in the ~10–12% range. Growth, however, appears driven primarily by concentrated capital allocators rather than broad organic demand, which introduces potential concentration risk if inflows reverse.

Overall, MainStreet can be characterized as a hybrid CeFi–DeFi yield infrastructure whose risk profile is driven less by smart contract risk and more by derivatives execution, margin dynamics, and redemption design under stress conditions. Continued transparency around leverage, coverage monitoring, clearing diversification, and redemption fairness mechanisms will be important factors in evaluating the protocol’s long-term resilience.

Related articles

TeloSkills: A Free Web3 Due Diligence Skill for Claude

Coinshift USPC & iUSPC - Comprehensive Due Diligence

MainStreet – Comprehensive Due Diligence

Introducing the Kinky IRM: Enhancing Interest Curves

Risk Curation Methodology for DeFi Yield Optimization

Meet IRMaster, The Effortless Interest Rate Manager for Liquity v2 & Forks

Stablecoins as Collateral: Pricing Guidelines

Coinshift USPC & iUSPC - Comprehensive Due Diligence